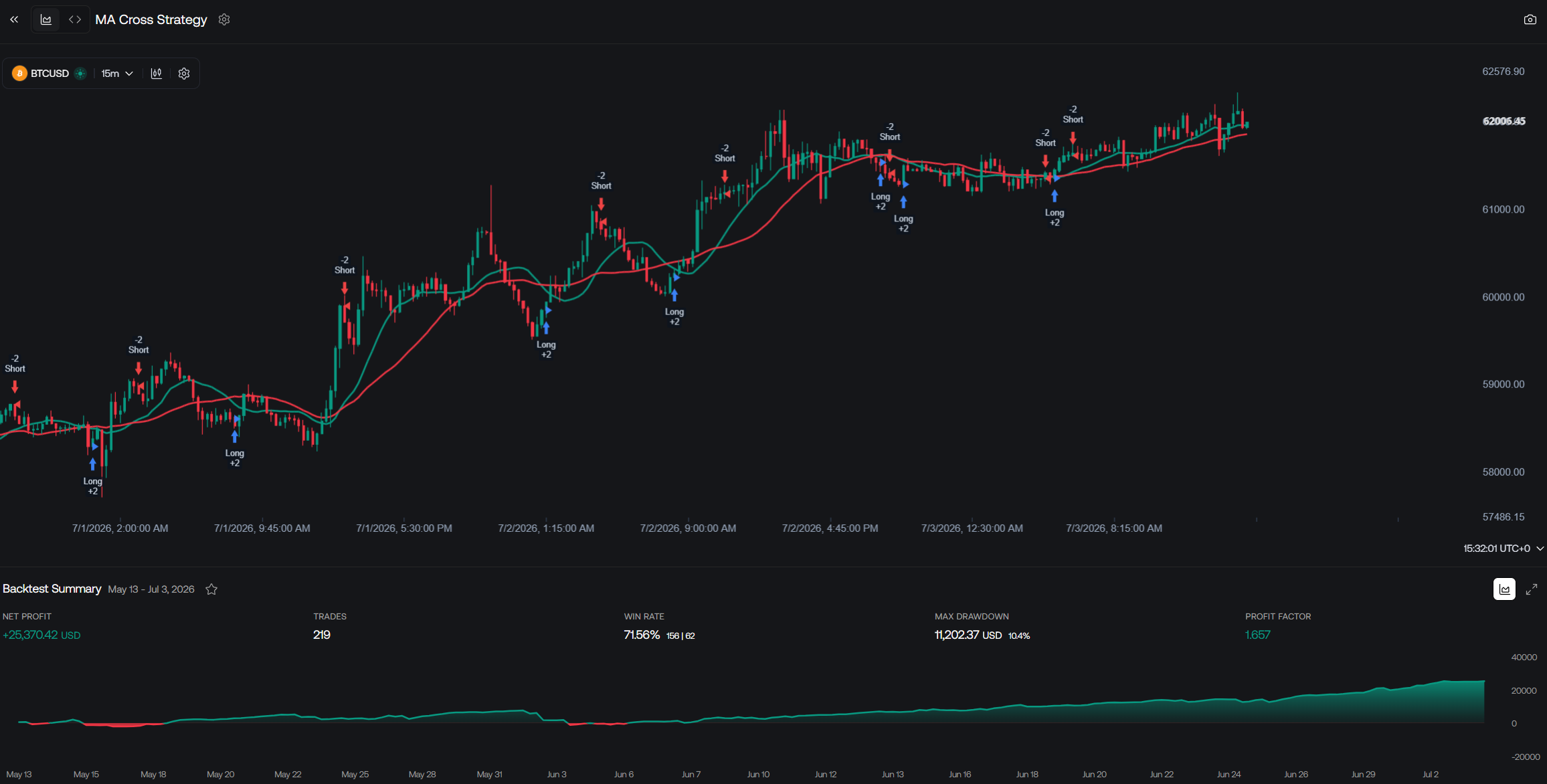

# Backtest Viewer (/docs/ai-backtesting/backtest-viewer)

Users have access to a wide variety of useful data and visualisations to evaluate a strategy trough the backtest viewer.

By default the backtest viewer will display backtest information from the most recent fetched strategy in the conversation.

You can check backtest results from previously fetched strategies by simply clicking on the card holding the strategy

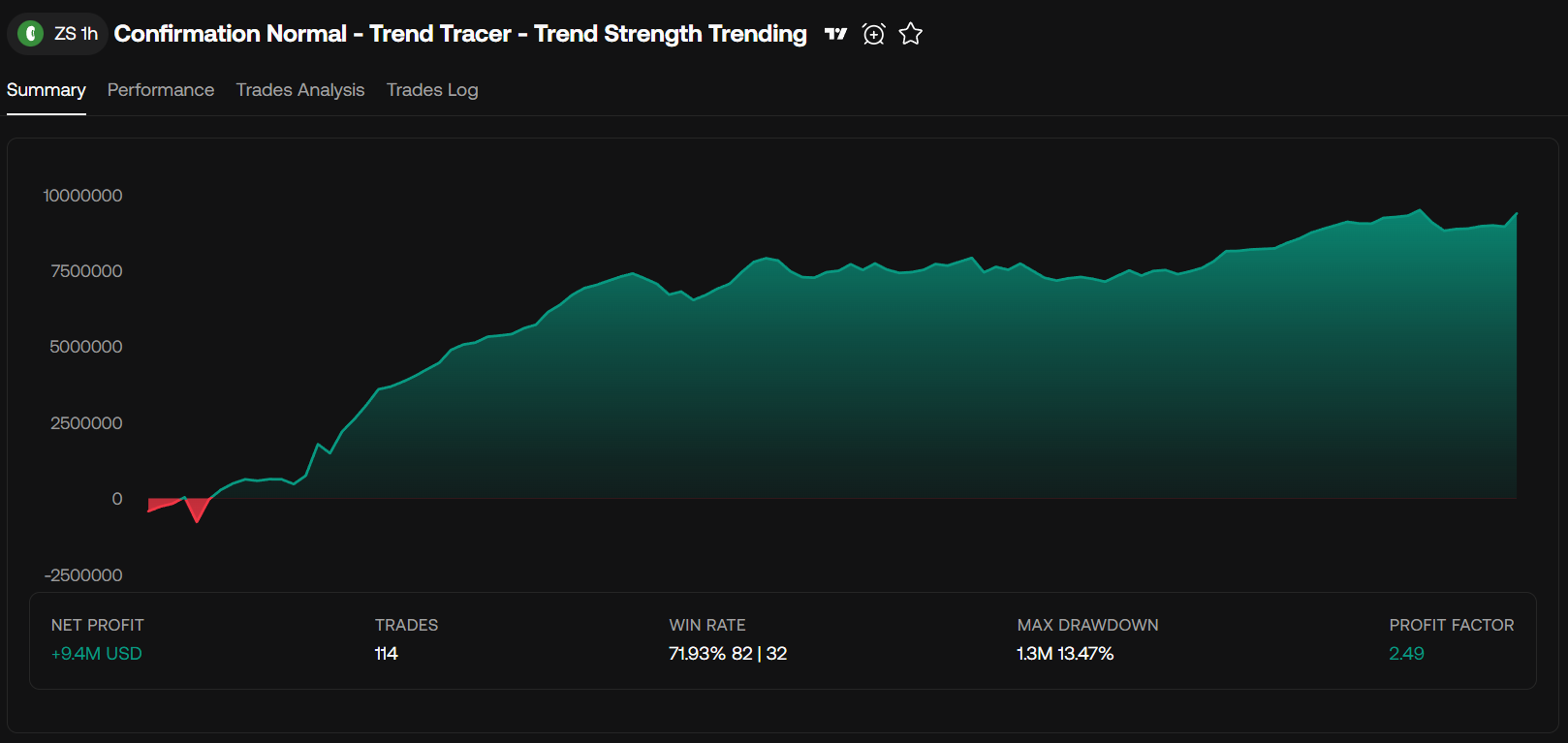

## Backtest Statistics [#backtest-statistics]

### Overview [#overview]

* Historical Net Profit

* Net Profit

* Trades

* Win Rate

* Winning Trades (left)

* Losing Trades (right)

* Max Drawdown

* Max Drawdown %

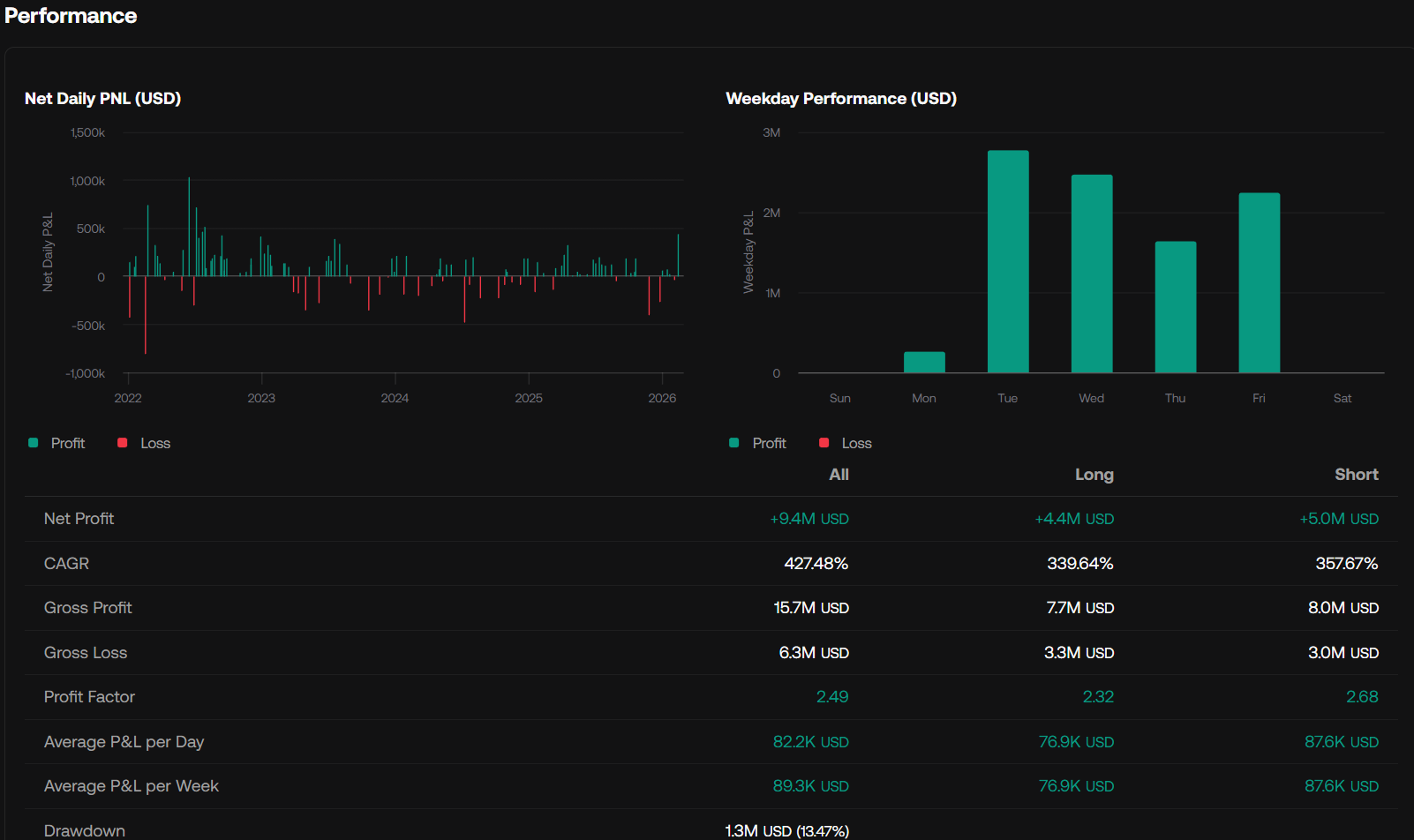

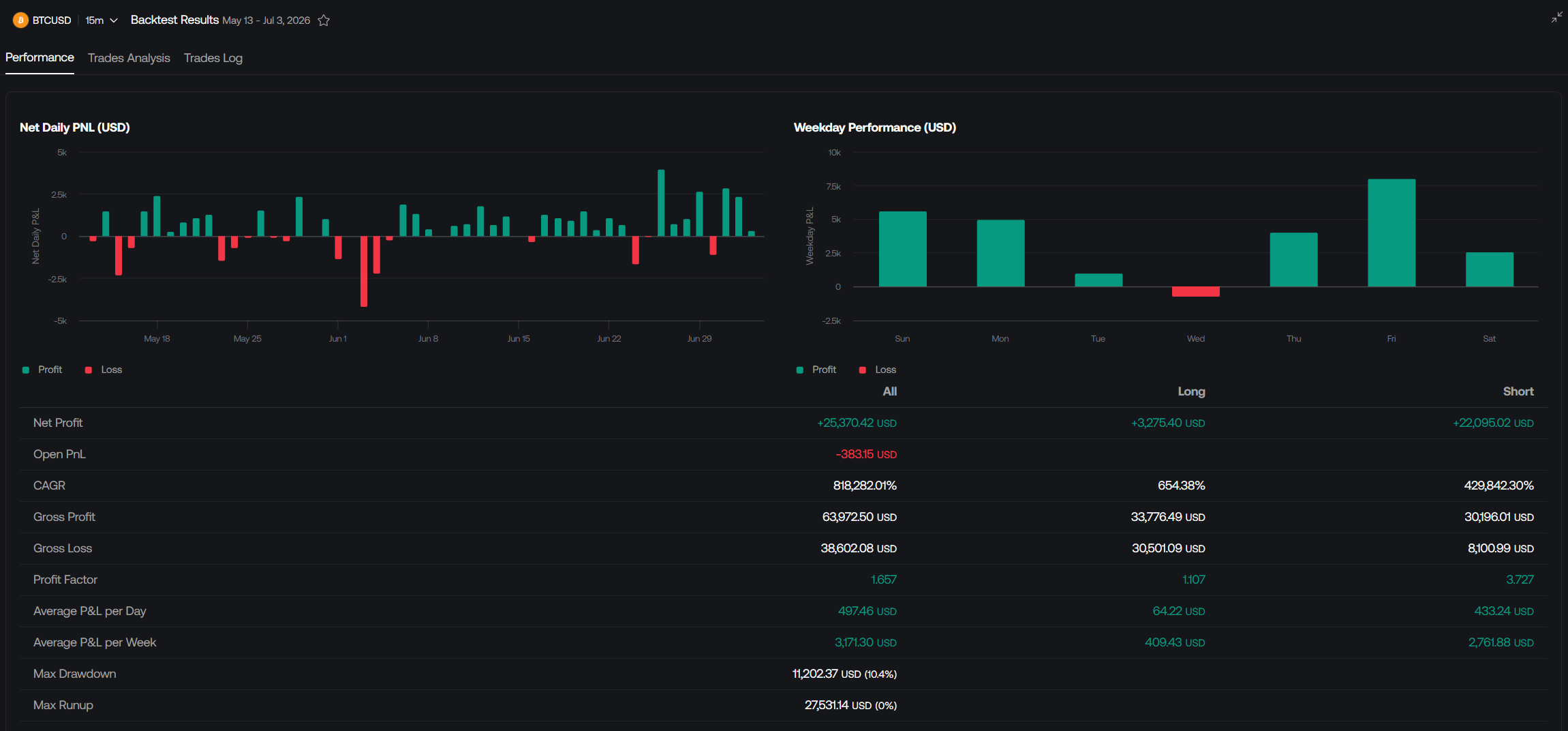

### Performance [#performance]

The **Performance** section includes two visualisations:

* Net Daily PNL: Net daily trades result (profit + loss)

* Weekday Performance: Sum of the profit and losses made during a specific day of the week

#### Table [#table]

A performance table is included listing statistics for all trades, only longs, and only shorts. The following statistics are returned:

*

Net Profit

*

CAGR (Compounded annualized growth rate)

*

Gross Profit

*

Gross Loss

*

Profit Factor

*

Average P&L per Day

*

Average P&L per Week

*

Drawdown

*

Drawdown Percent

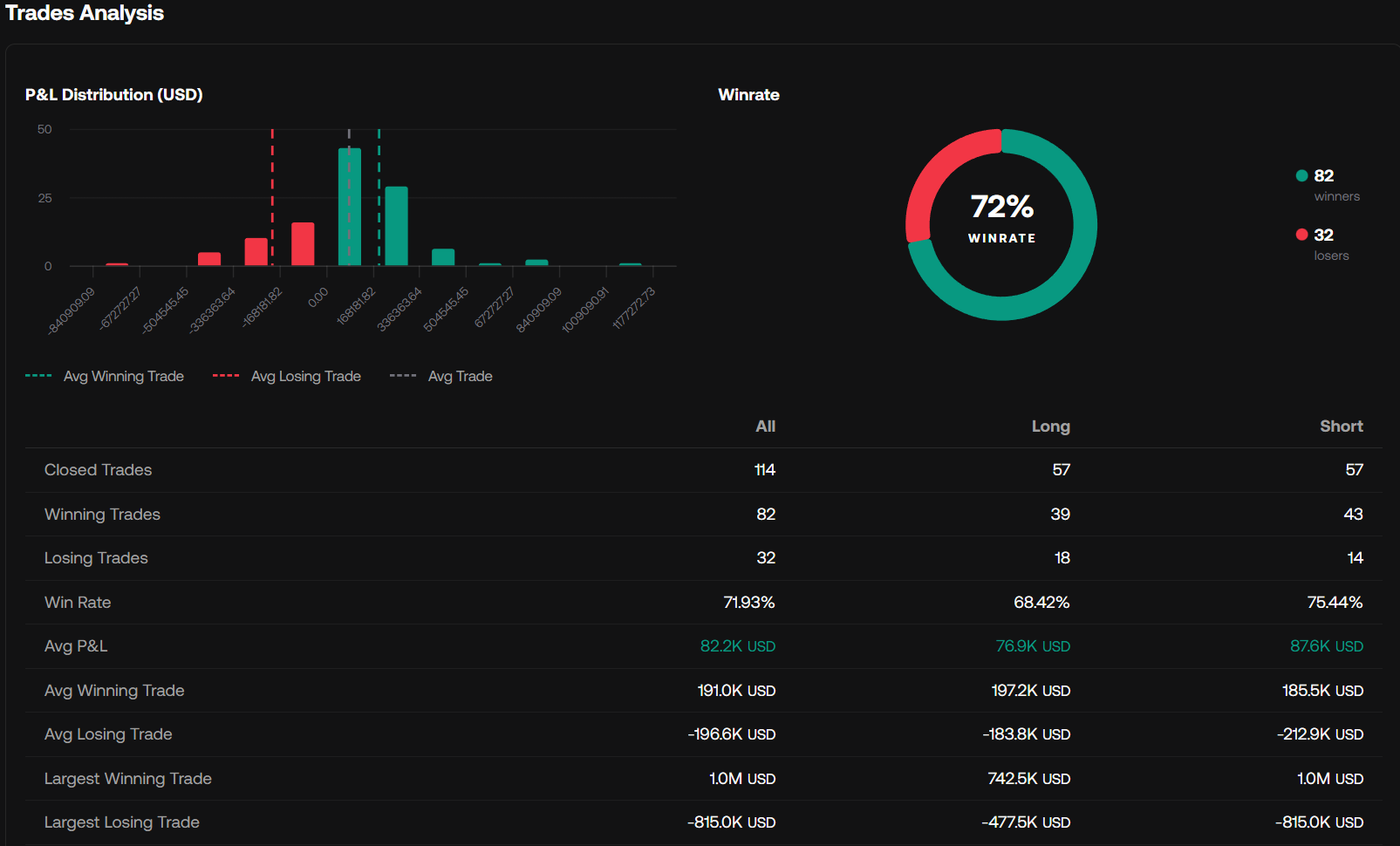

### Trades Analysis [#trades-analysis]

The **Trades Analysis** section includes two visualisations:

* P\&L Distribution: Distribution of trade profit and losses

* Winrate: Shows winrate, winning trades and losing trades

* Duration vs P\&L: Scatter plot showing trade duration (in bars) against the trade result

#### Table [#table-1]

A trades analysis table is included listing statistics for all trades, only longs, and only shorts. The following statistics are returned:

*

Closed Trades

*

Winning Trades

*

Losing Trades

*

Win Rate

*

Avg P&L

*

Avg Winning Trade

*

Avg Losing Trade

*

Largest Winning Trade

*

Largest Losing Trade

#### Duration [#duration]

A duration table is included listing statistics for all trades, only longs, and only shorts. The following statistics are returned:

*

Avg Trade Duration (bars)

*

Avg Winning Trade Duration (bars)

*

Avg Losing Trade Duration (bars)

*

Avg Trades per Day

*

Avg Trades per Week

*

Longest Trade (bars)

*

Shortest Trade (bars)

*

Longest Winning Streak (bars)

*

Longest Losing Streak (bars)

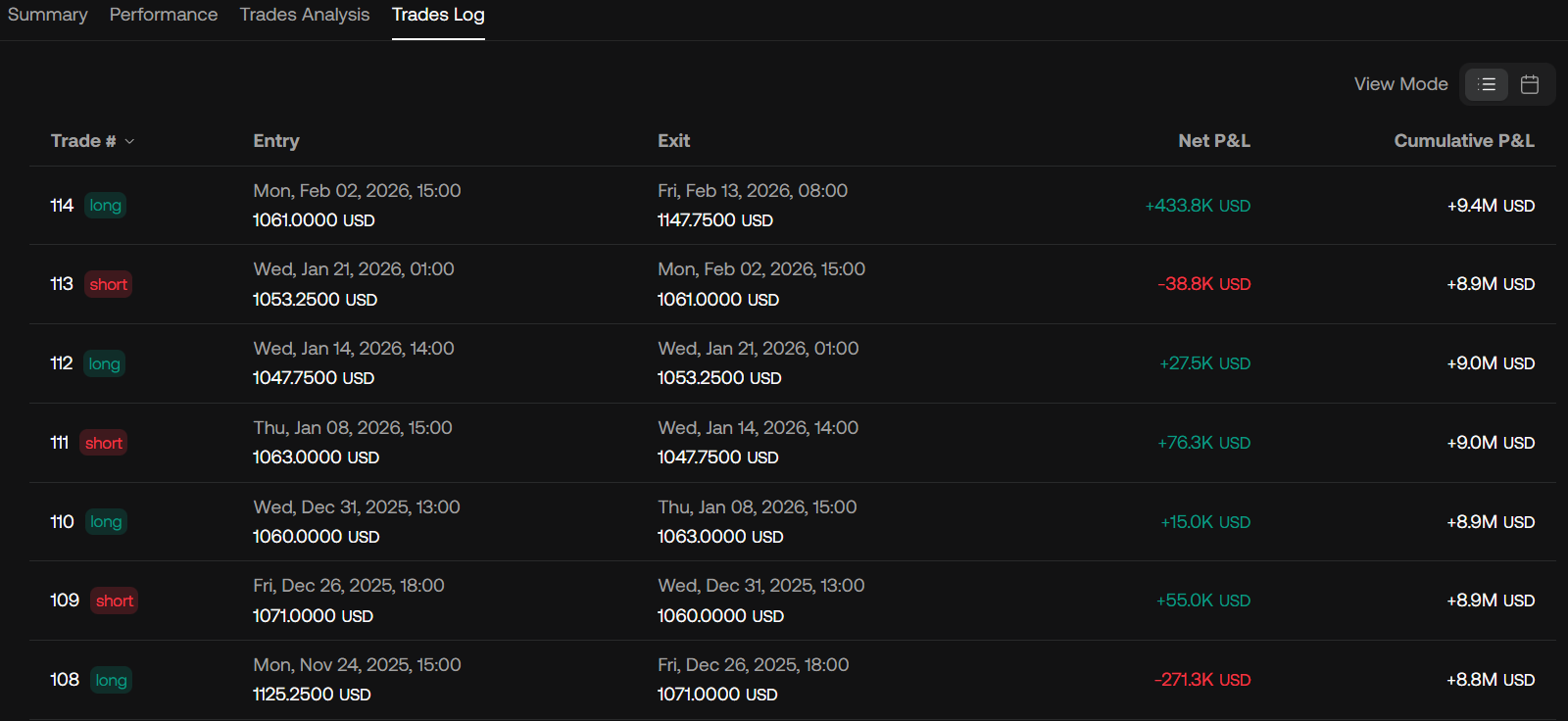

## Trades Log [#trades-log]

A trades log table is included showing each closed trade in chronological order, including the trade number, trade side, entry, exit, net P\&L, and the running cumulative P\&L after each trade.

Click on a column to sort it ascendingly or descendingly.

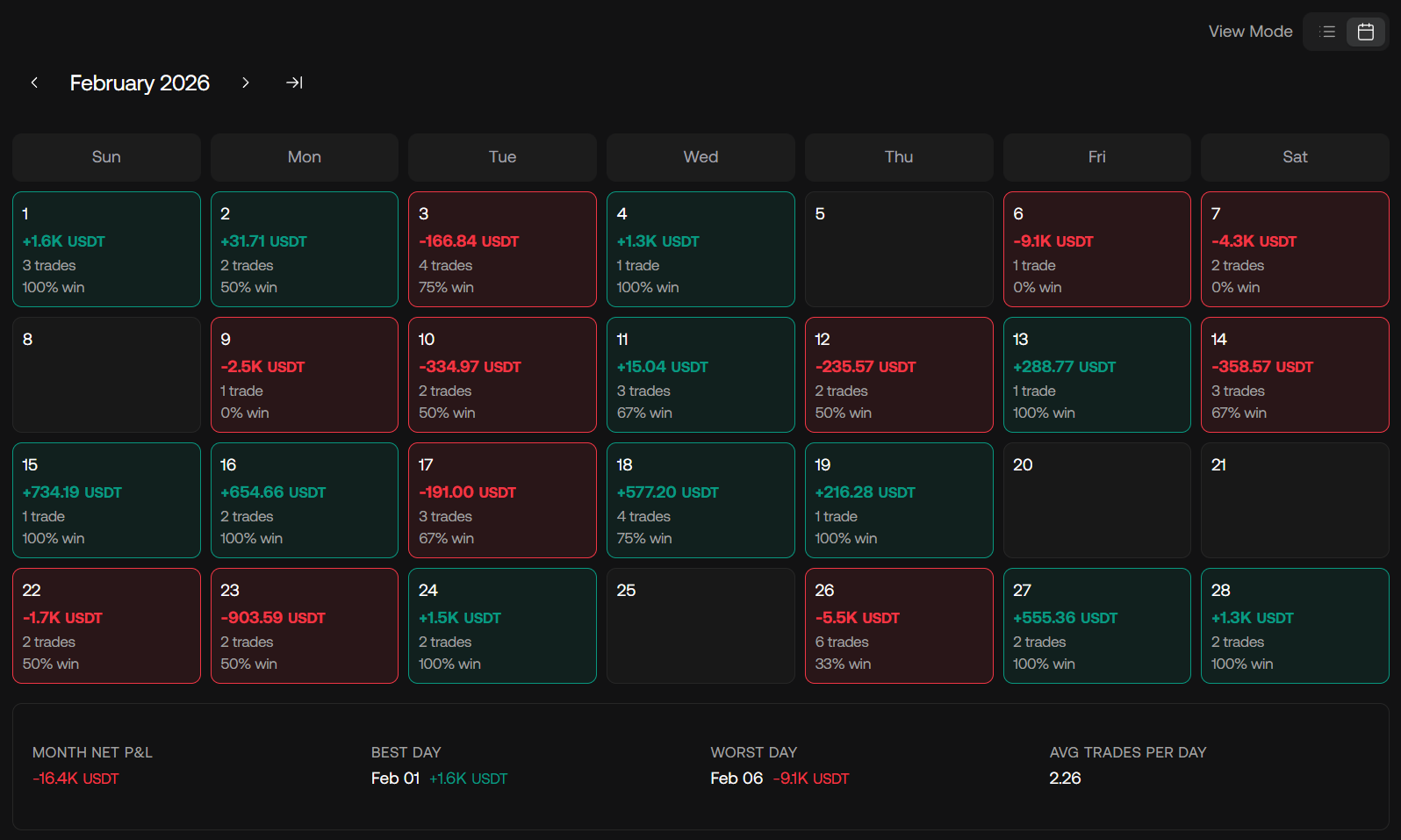

### Calendar View [#calendar-view]

When the `View Mode` is switched to calendar view, trades are grouped by day in a monthly layout with month navigation at the top. Each day can show its net P\&L, number of trades, and win rate, while a summary below highlights the month net P\&L, best day, worst day, and average trades per day.

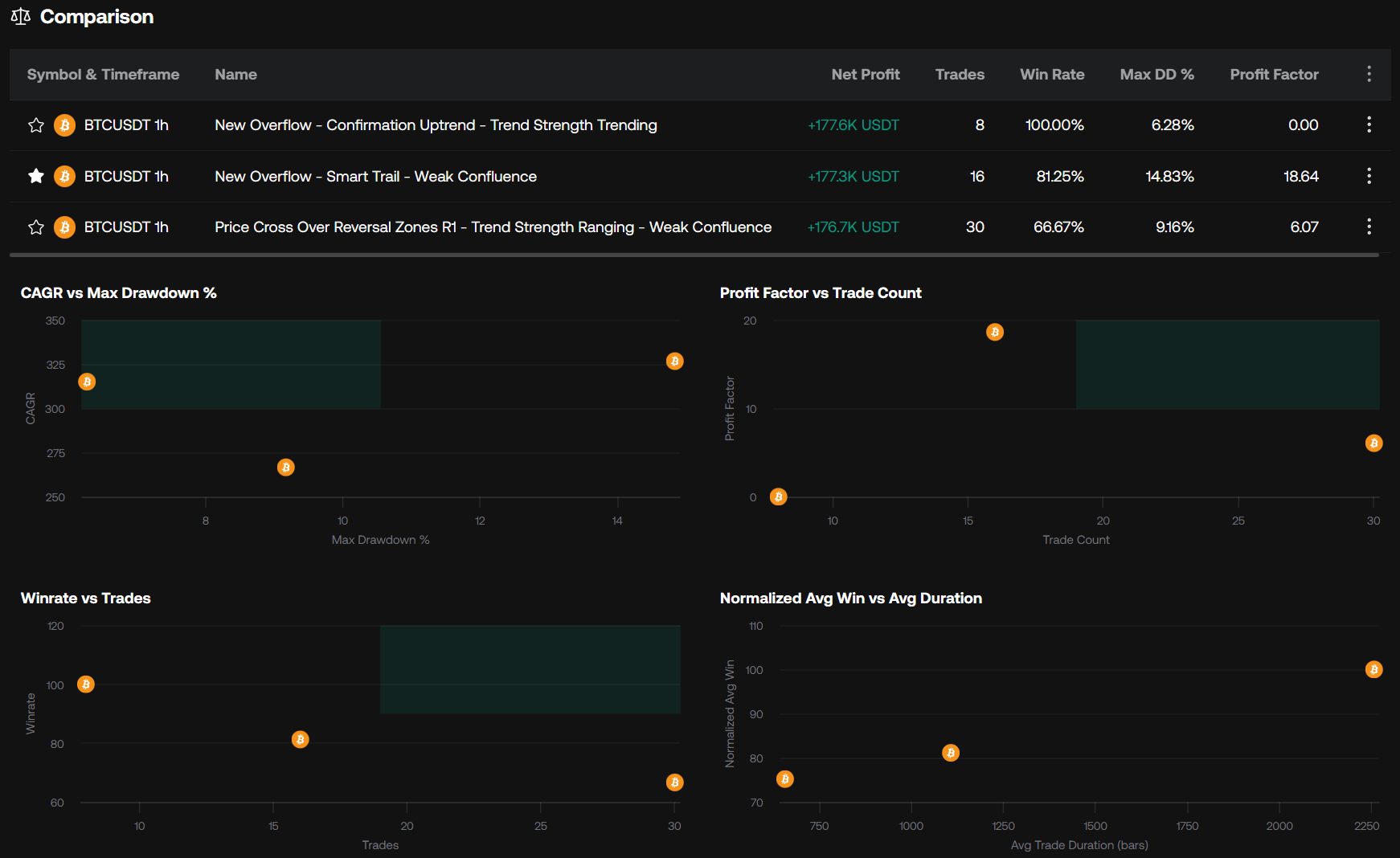

## Strategy Comparison View [#strategy-comparison-view]

When the Backtesting AI fetches multiple strategies at once, these will eb displayed in a comparison view, allowing for detailed comparisons.

### Comparison Table [#comparison-table]

The comparison table displays each strategy side by side, including the symbol and timeframe, strategy name, net profit, trades, win rate, max DD %, and profit factor.

### Comparison Scatter Plots [#comparison-scatter-plots]

The comparison scatter plots help visualize how strategies relate across key metrics, with views such as CAGR vs Max Drawdown %, Profit Factor vs Trade Count, Winrate vs Trades, and Normalized Avg Win vs Avg Duration.

Each point represents a strategy, with strong performers being located in the quadrant in green.

Hovering over a strategy point in the graph shows a tooltip with the relevant strategy details.

# Fetching Information (/docs/ai-backtesting/fetching-information)

The AI Backtesting Assistant is able to fetch our product documentation to provide relevant information to you about the features used by a retrieved strategy or to simply help you learn more about our products.

The AI will automatically determine whether it requires fetching context from the documentation depending on the user query.

You can force the AI to fetch information from the documentation by telling it to fetch the documentation.

For example:

> Tell me more about confirmation signals, use the documentation

This can prevent the AI from giving partial information he might know from his existing context window.

## Detailed Strategy Descriptions Using Docs [#detailed-strategy-descriptions-using-docs]

We can request for the AI to provide important context about the conditions returned by a trading strategy.

## Using Docs to Get Tailored Strategies [#using-docs-to-get-tailored-strategies]

By asking the AI to learn more about the LuxAlgo features from the documentation, we can effectively get unique trading strategies by simply mentioning trading styles.

For example, we can use the following prompt:

> From the documentation search for the best features for swing trading, then find a strategy using those features that provides good results on crypto on the hourly timeframe

# Fetching Strategies (/docs/ai-backtesting/fetching-strategies)

The primary role of the AI Backtesting Assistant is to help users find strategies quickly without having to manually iterate through various conditions, tickers, and timeframes on TradingView charts. Instead, users can simply ask the AI to look for the strategy that would best match the criteria they want.

The AI Backtesting Assistant has access to millions of unique strategies, each made using a wide variety of conditions.

This AI tool’s backtesting data & analytics are for informational purposes only and do not constitute financial advice or recommendations to buy or sell any financial product, including but not limited to securities, derivatives, cryptocurrencies, or other investment instruments.

This tool may contain errors, and past performance is not indicative of future results. Always conduct your own research and consult with a professional financial advisor.

LuxAlgo is not liable for any decisions made based on any information given. Read our [full disclaimer](https://www.luxalgo.com/legal/disclaimer/).

## Strategies Configuration [#strategies-configuration]

Strategies are evaluated using a maximum of the most recent 20.000 bars, with an initial capital of 10.000 base currency, without commissions/slippage, and using default settings for all toolkits features.

Unit position sizing is used across all tickers.

When a strategy enters a trade, any previous trade is closed. As such, it is not possible for two positions to be open at the same time.

Strategies do not make use of stop losses or take profits.

See the section below to learn more about the supported tickers, timeframes, and backtesting conditions.

### Schedule [#schedule]

In order to preserve ressources and avoid redundancy we run backtests three times a week:

* **Monday** 23:30 UTC

* **Wednesday** 23:30 UTC

* **Friday** 23:30 UTC

### Supported Tickers [#supported-tickers]

The following tickers are supported:

* AAPL

* AMD

* AMZN

* BABA

* CELH

* COIN

* CRWD

* DIS

* DUOL

* GME

* GOOG

* HOOD

* INTC

* MA

* META

* MSFT

* MSTR

* NFLX

* NKE

* NVDA

* ORCL

* PLTR

* PYPL

* RIVN

* SMCI

* SNOW

* SOFI

* TSLA

* UBER

* WMT

* ARKK

* IWM

* QQQ

* SPY

* VTI

* AAVEUSDT (Binance)

* ADAUSDT (Binance)

* ATOMUSDT (Binance)

* AVAXUSDT (Binance)

* BCHUSDT (Binance)

* BNBUSDT (Binance)

* BTCUSDT (Binance)

* DOGEUSDT (Binance)

* DOTUSDT (Binance)

* EOSUSDT (Binance)

* ETHUSDT (Binance)

* HBARUSDT (Binance)

* HYPEUSD (Kucoin)

* JUPUSDT (Binance)

* KASUSD (Kucoin)

* LINKUSDT (Binance)

* LTCUSDT (Binance)

* POLUSDT (Binance)

* SHIBUSDT (Binance)

* SOLUSDT (Binance)

* SUIUSDT (Binance)

* TONUSDT (Binance)

* TRXUSDT (Binance)

* UNIUSDT (Binance)

* VETUSDT (Binance)

* XLMUSDT (Binance)

* XRPUSDT (Binance)

* AUDJPY

* AUDUSD

* EURAUD

* EURGBP

* EURUSD

* EURJPY

* GBPAUD

* GBPJPY

* GBPUSD

* NZDUSD

* USDCAD

* USDCHF

* USDJPY

* XAGUSD

* XAUUSD

* UKOIL

* NQ

* ES

* RTY

* YM

* GC

* SI

* CL

* NG

* PL

* ZC

* ZW

* ZS

* 6E

* 6J

US equities (Stocks and ETFs) data is sourced from Cboe BZX and use regular trading hours.

Futures are based on continuous contracts and use electronic trading hours, without adjustment for contracts changes. Additionally, unlike TradingView, Futures contracts roll on the day prior to expiration.

### Supported Timeframes [#supported-timeframes]

5m, 15m, and 60m timeframes are supported.

## Strategy Entry and Exits Constructions [#strategy-entry-and-exits-constructions]

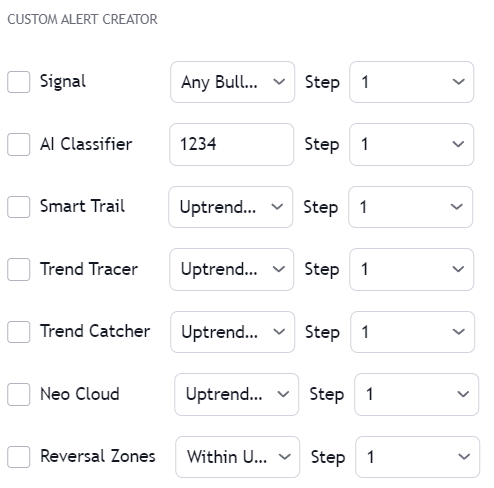

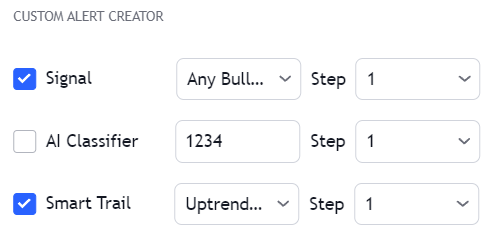

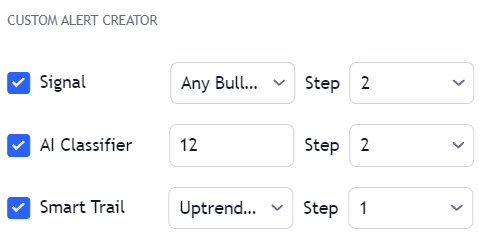

Strategy entry conditions can make use of multiple conditions from different toolkits together. We classify conditions as triggers and filters:

* Triggers: Triggers determine the initial conditions used by a strategy. These tend to be less persistent events on a chart, occurring for a single bar.

* Filters: Filters add precision to a strategy, potentially filtering out bad trades that would have been taken by simply using triggers. Filters tend to be more persistent, lasting for multiple bars on a chart.

Entry conditions contain a single trigger, and can contain up to two filters.

It is possible for a long/short entry condition to contain both bullish and bearish conditions

Long and short entry conditions mirror each other, that is, if the long entry condition uses a bullish condition, the short entry condition will use the same condition but bearish.

Example:

> * long: **Confirmation Any Bullish** and **Bullish Smart Trail** and **Bearish Trend Tracer**

> * short: **Confirmation Any Bearish** and **Bearish Smart Trail** and **Bullish Trend Tracer**

Finally, it is possible that some strategies using conditions from the Signals & Overlays® toolkit use exits condition to close trades.

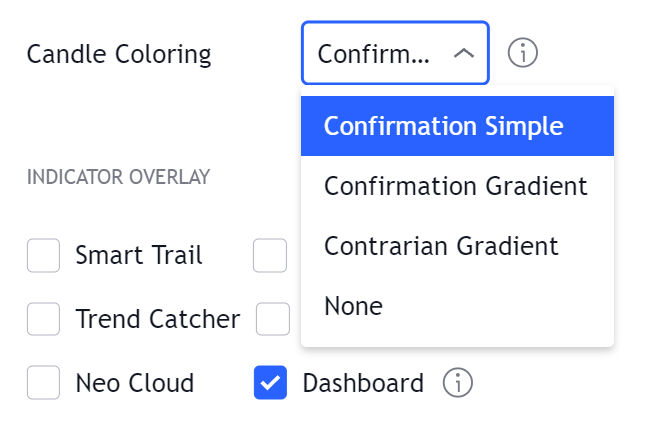

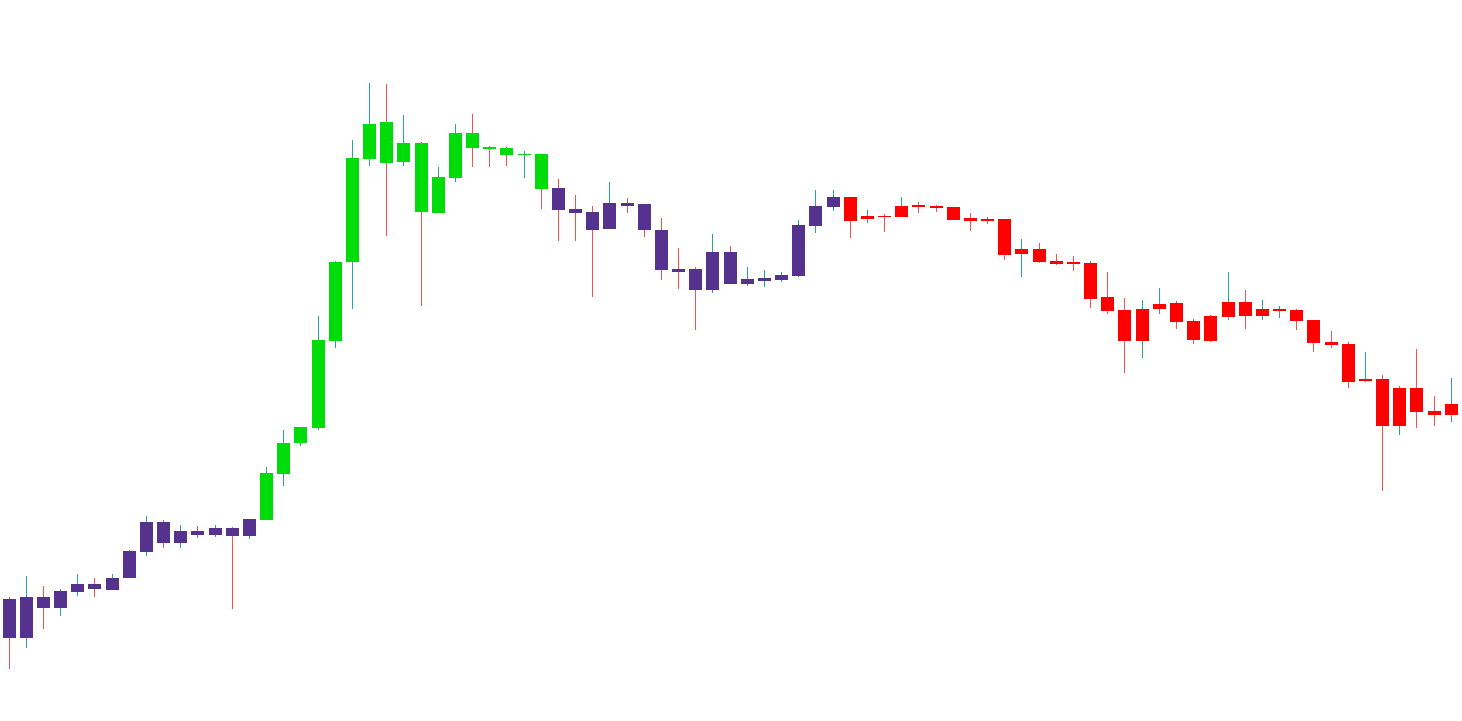

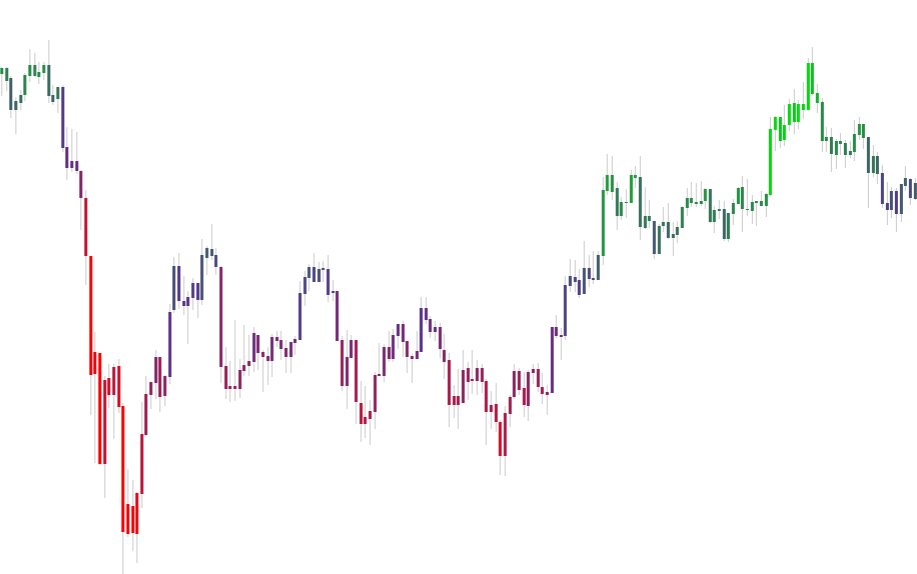

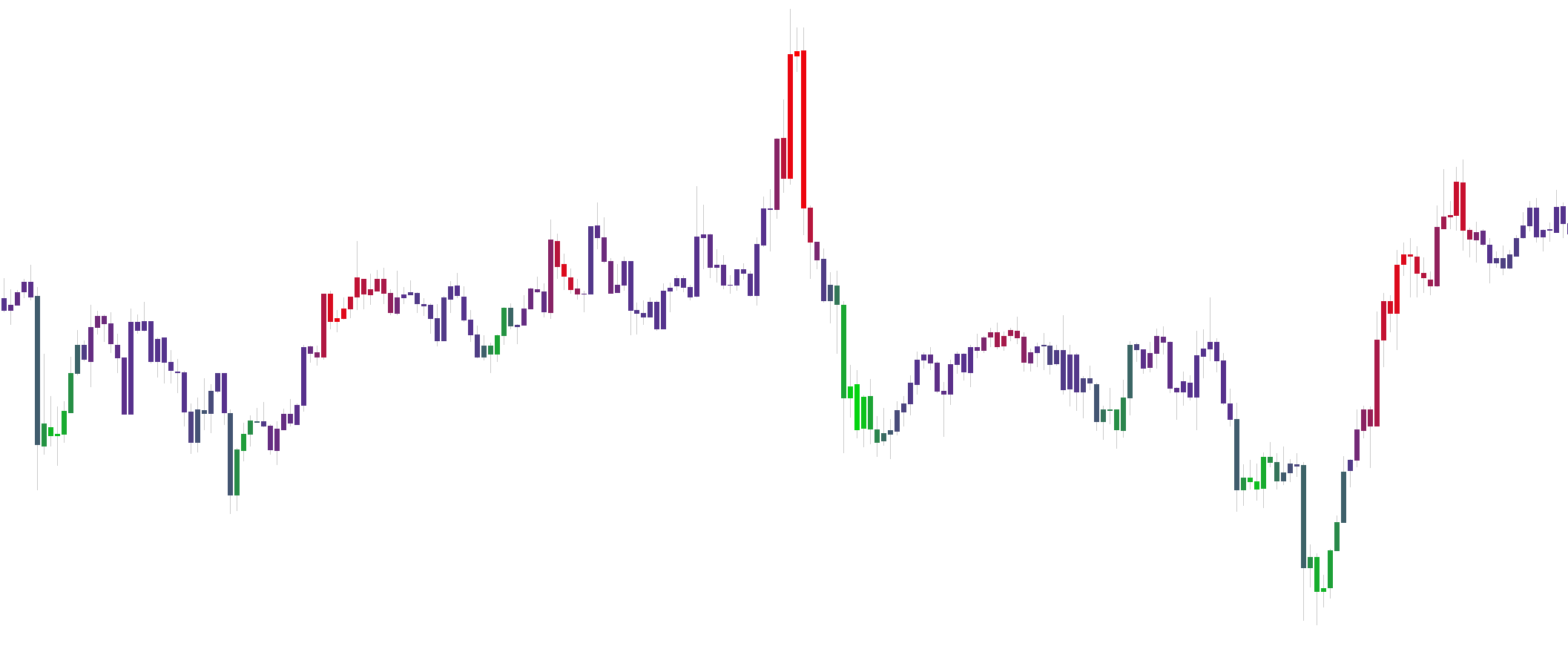

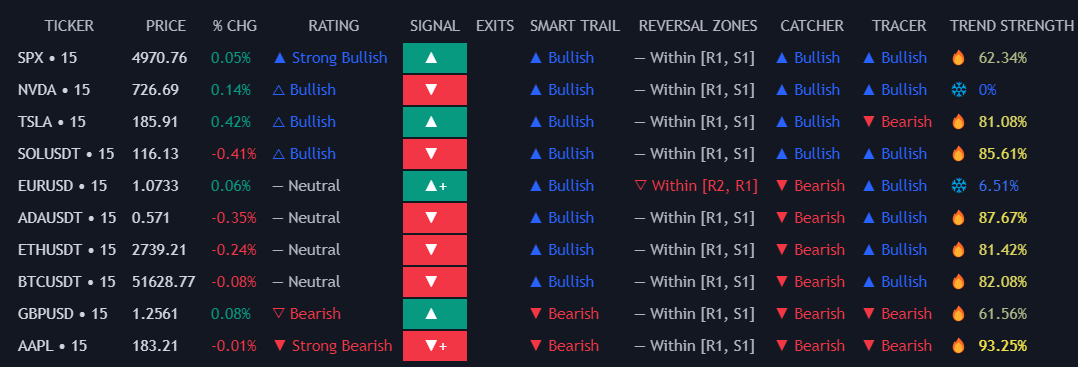

### Signals & Overlays® Conditions [#signals--overlays-conditions]

***

#### Triggers [#triggers]

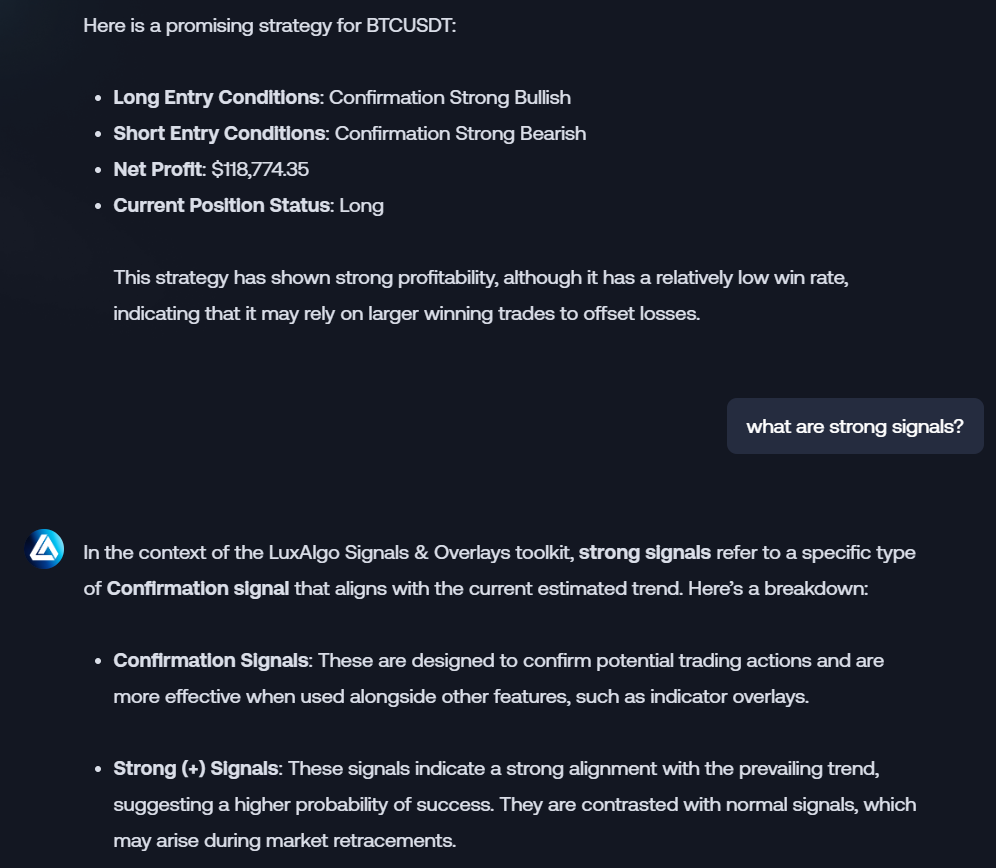

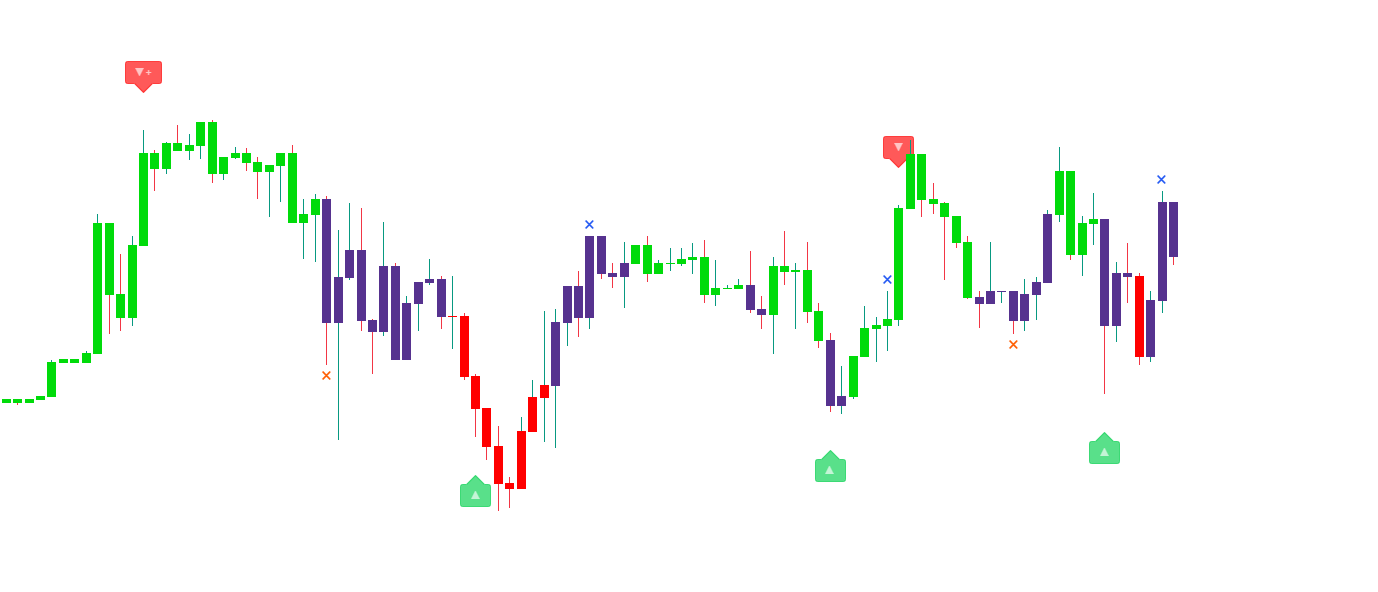

* Confirmation Any Bullish

* Confirmation Normal Bullish

* Confirmation Strong Bullish

* Contrarian Any Bullish

* Contrarian Normal Bullish

* Contrarian Strong Bullish

* Smart Trail Switch Bullish

* Price Cross Under Reversal Zones S1

* Trend Tracer Switch Bullish

* Trend Catcher Switch Bullish

* Neo Cloud Switch Bullish

* Confirmation Any Bearish

* Confirmation Normal Bearish

* Confirmation Strong Bearish

* Contrarian Any Bearish

* Contrarian Normal Bearish

* Contrarian Strong Bearish

* Smart Trail Switch Bearish

* Price Cross Over Reversal Zones R1

* Trend Tracer Switch Bearish

* Trend Catcher Switch Bearish

* Neo Cloud Switch Bearish

#### Filters [#filters]

* Confirmation Uptrend

* Contrarian Uptrend

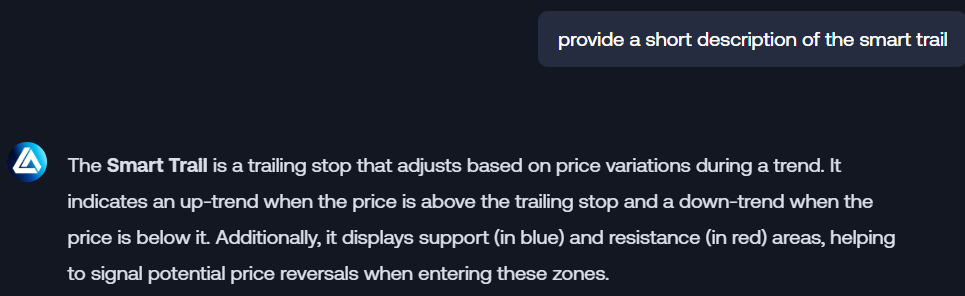

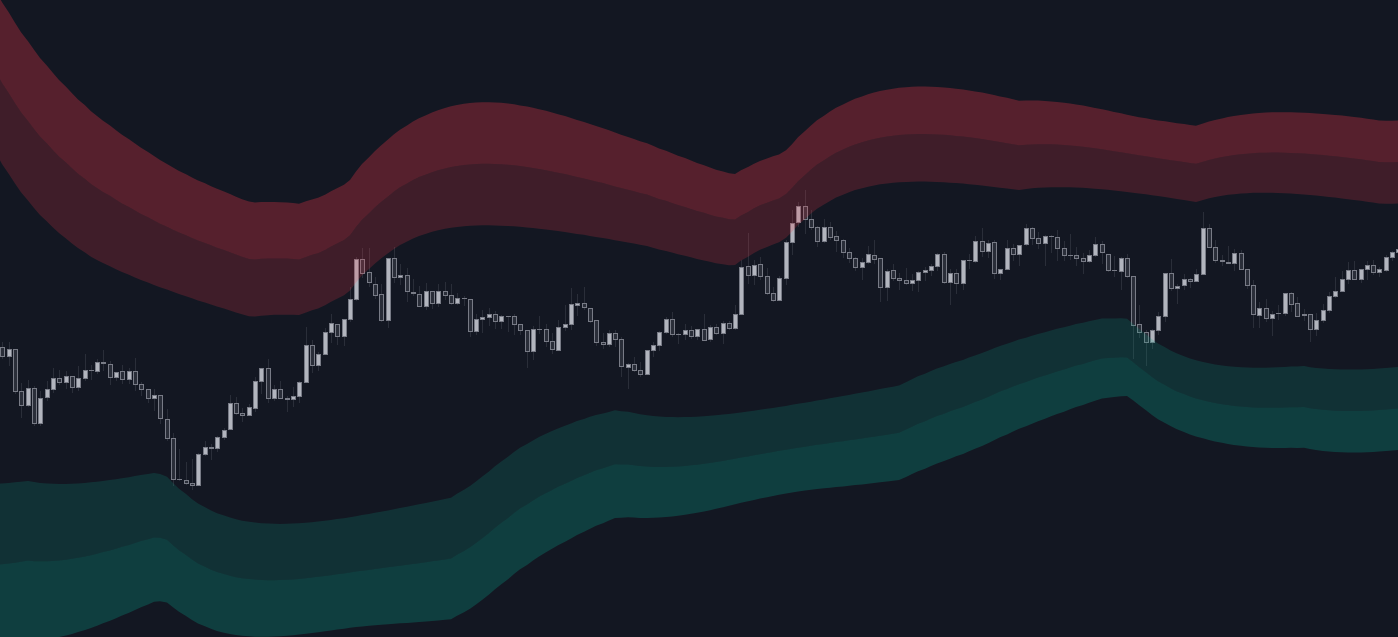

* Bullish Smart Trail

* Price Below Reversal Zones S1

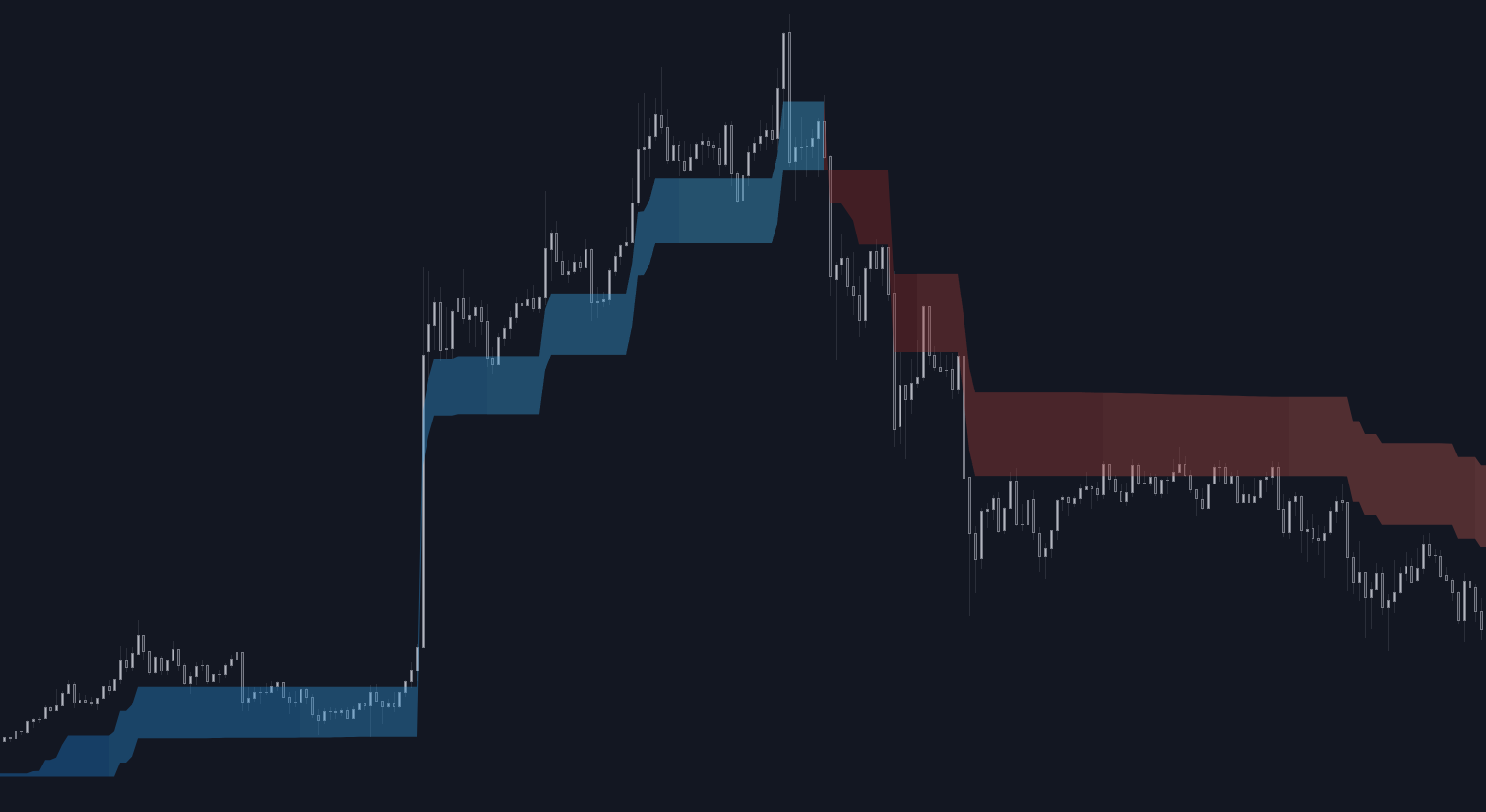

* Trend Tracer Bullish

* Trend Catcher Bullish

* Neo Cloud Bullish

* Confirmation Downtrend

* Contrarian Downtrend

* Bearish Smart Trail

* Price Above Reversal Zones R1

* Trend Tracer Bearish

* Trend Catcher Bearish

* Neo Cloud Bearish

* Trend Strength Trending

* Trend Strength Ranging

#### Exits [#exits]

Strategies using the Signals & Overlays® toolkit can make exit trades which are outlined below:

* Any strategy using Confirmation Signals can make use of builtin-exits labelled as "Confirmation Built-in Exits".

* Any strategy using Contrarian Signals can make use of builtin-exits labelled as "Contrarian Builtin Exits".

* Any strategy using Reversal Zones can make use of the exit condition "Price Cross R1/S1 Average", which will exit a trade when price crosses the average of the Reversal Zones.

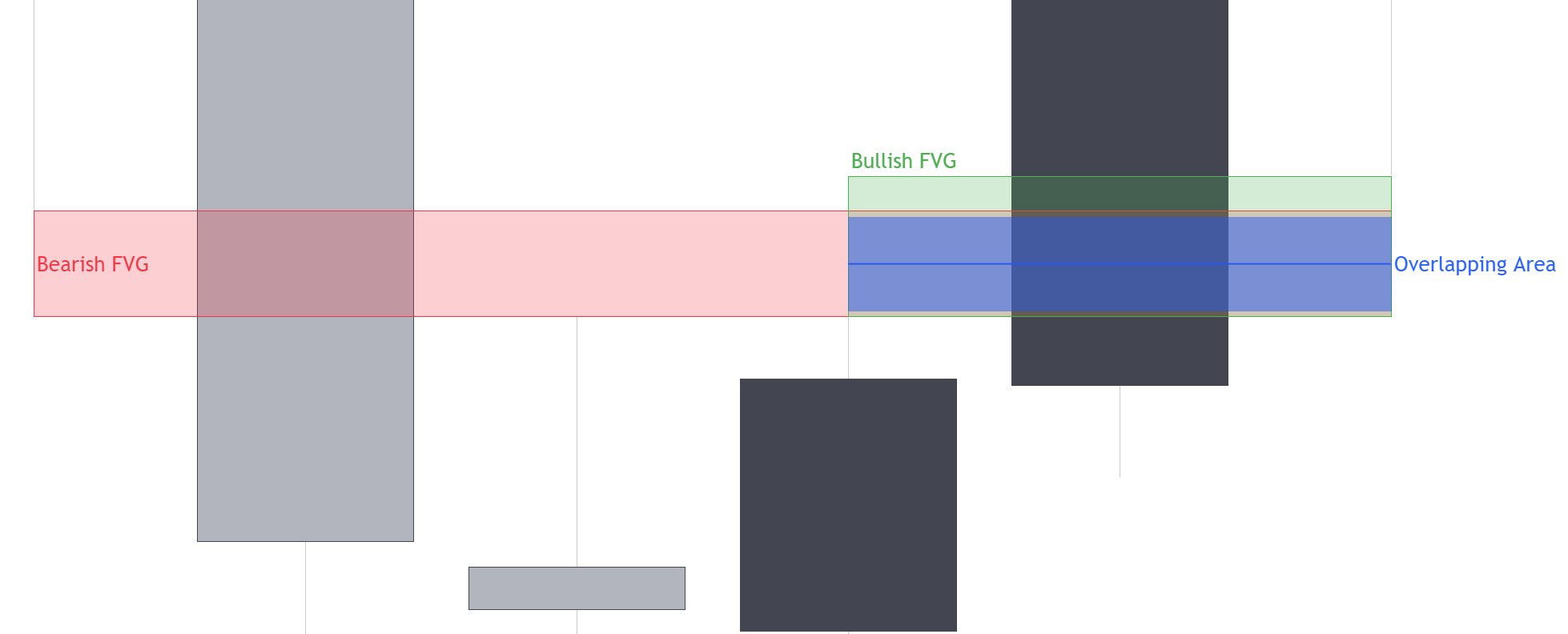

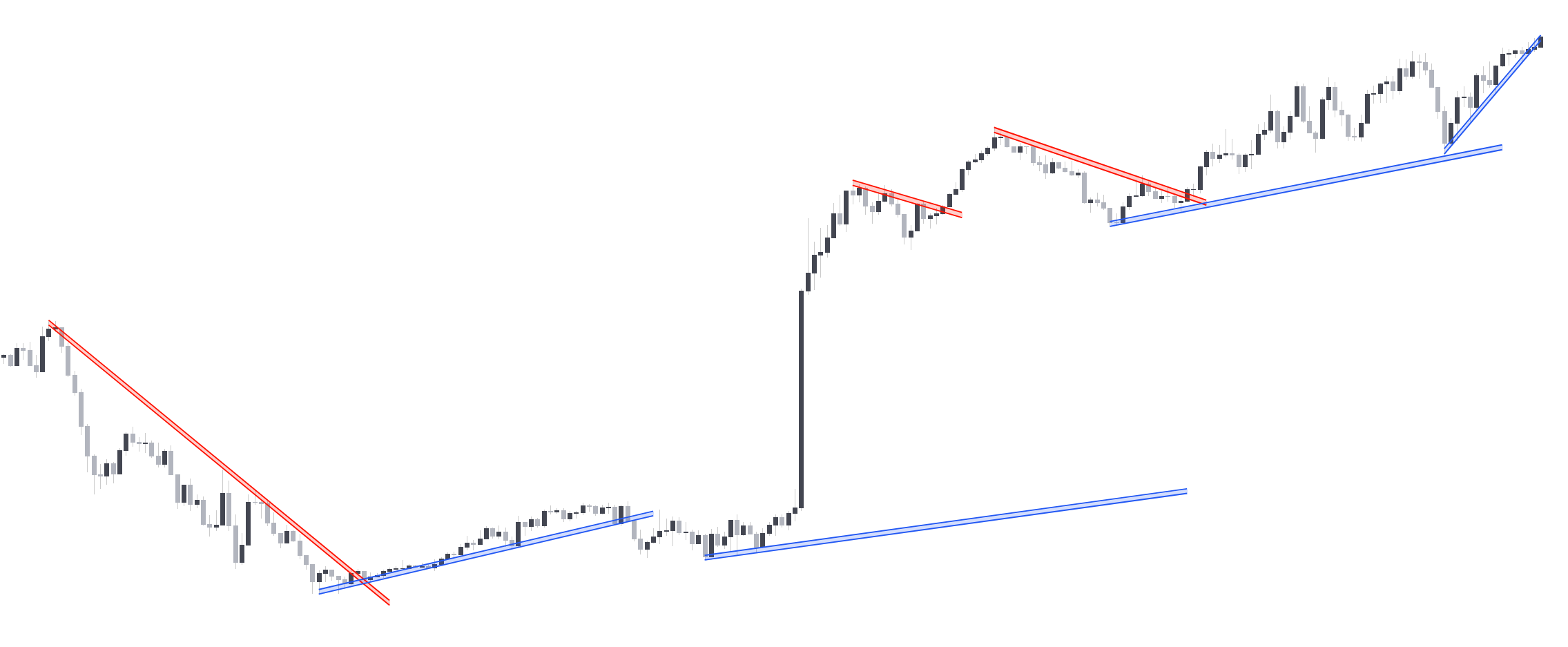

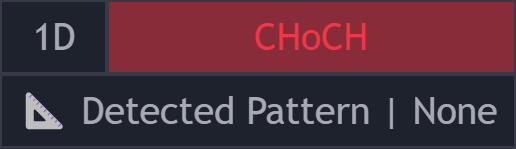

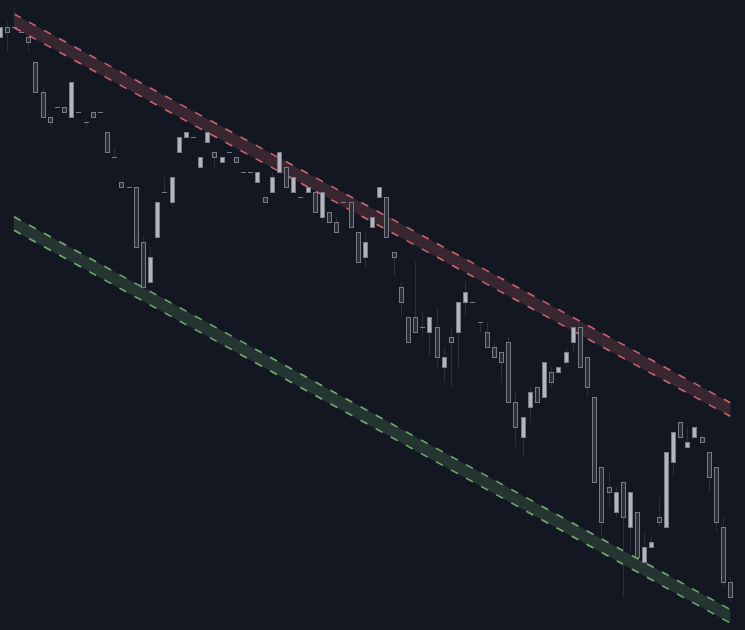

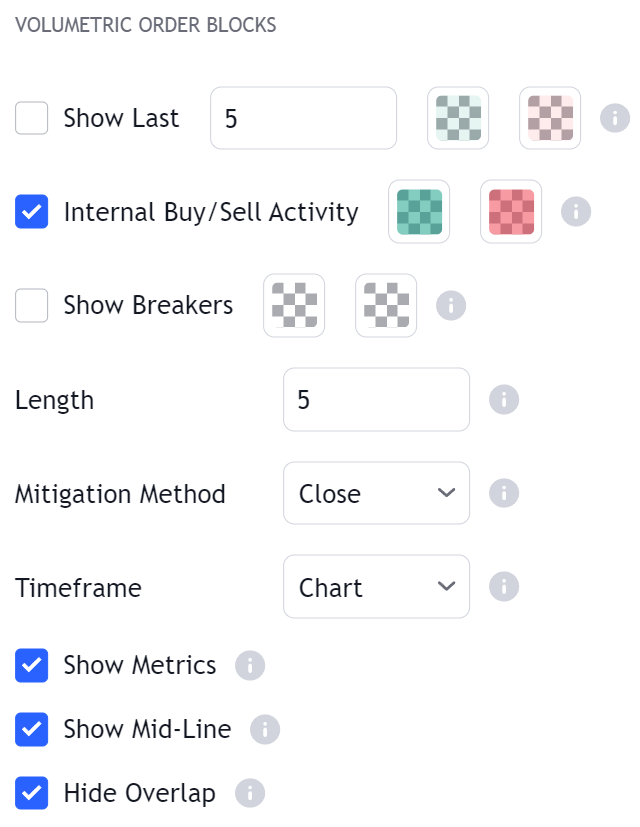

### Price Action Concepts® Conditions [#price-action-concepts-conditions]

***

Currently only triggers are supported for the Price Action Concepts® toolkit.

#### Triggers [#triggers-1]

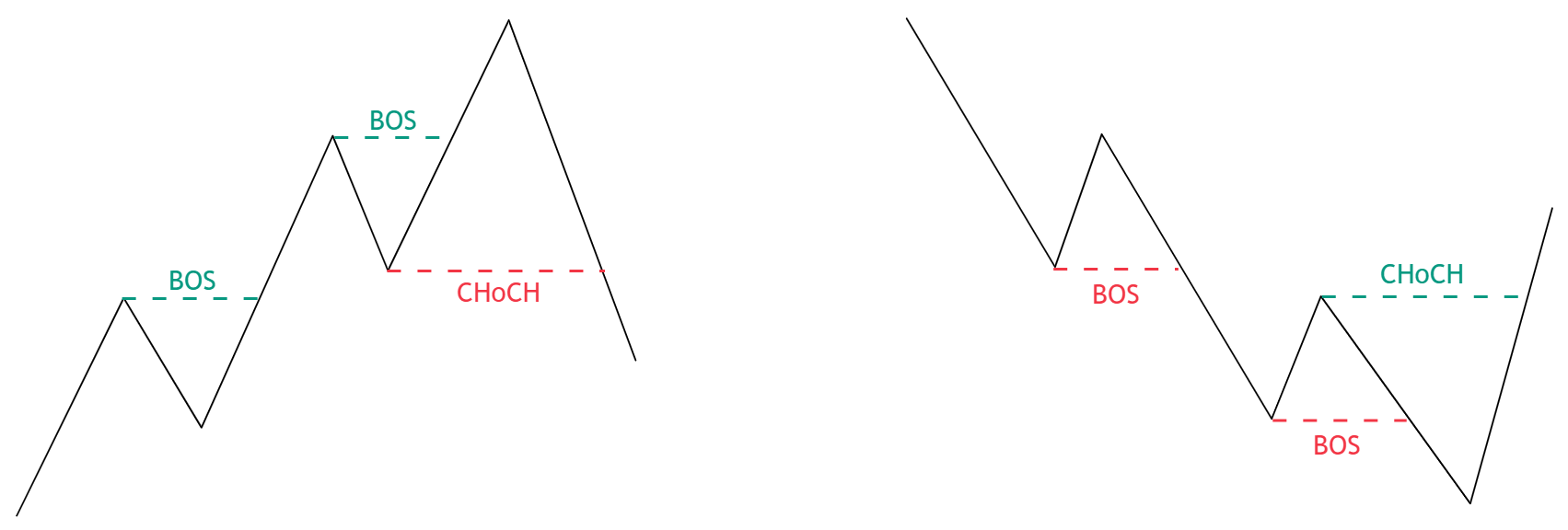

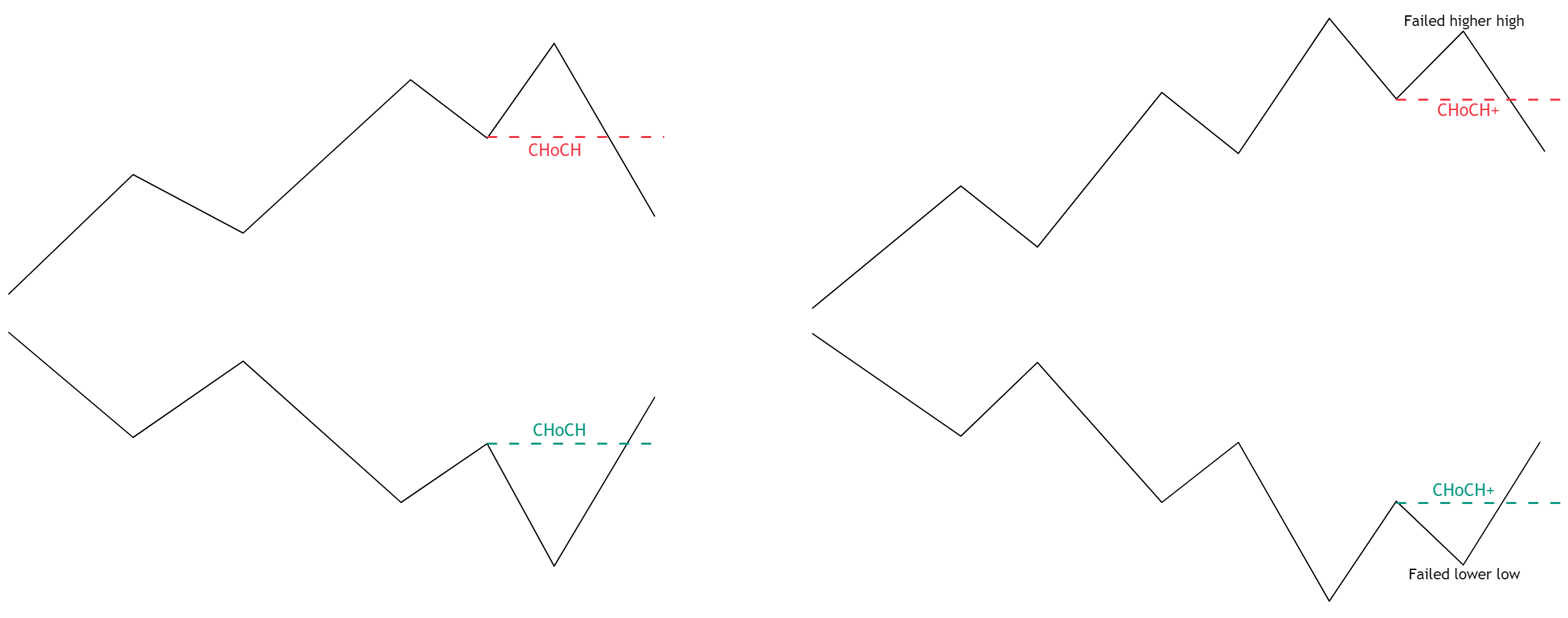

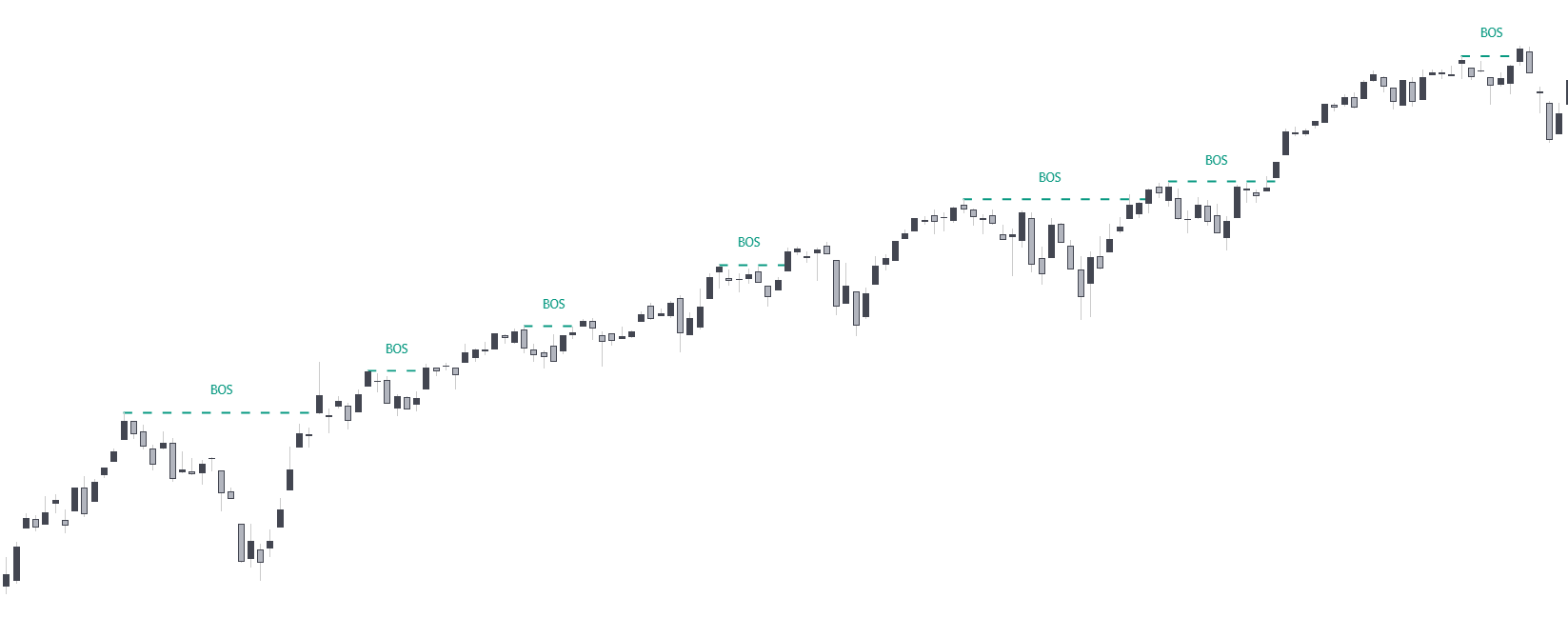

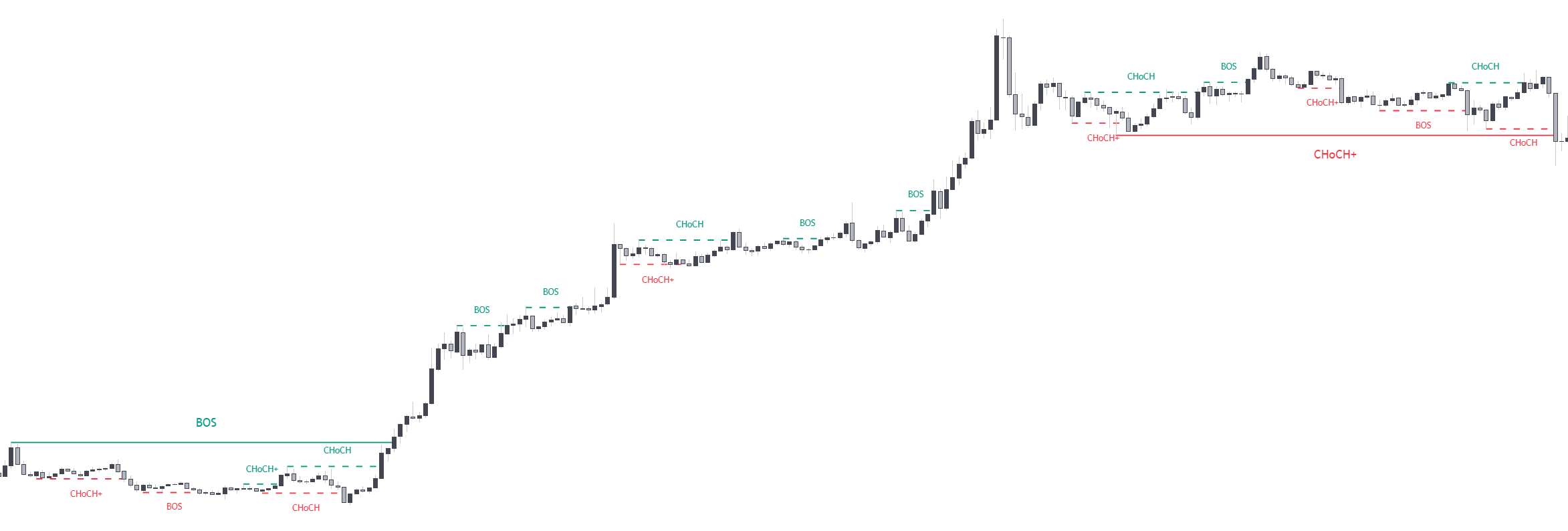

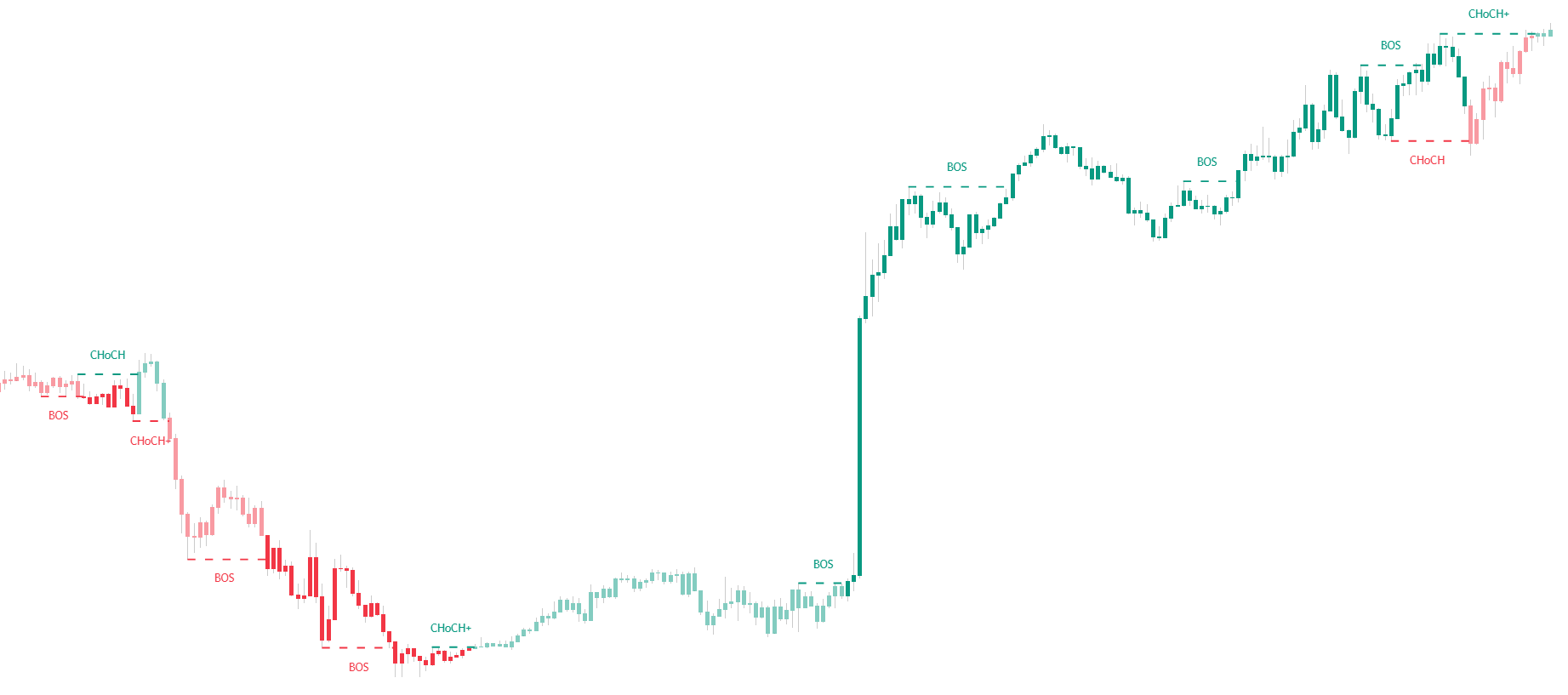

* Bullish CHoCH

* Bullish BOS

* Bullish OB Entered

* Bullish OB Exited

* New Bullish FVG

* Bearish FVG Mitigated

* New Bullish Opening Gap

* Bearish Opening Gap Mitigated

* New Bullish Volume Imbalance

* Bearish Volume Imbalance Mitigated

* Bullish Liquidity Grab

* Bearish Trendline Break

* Bearish CHoCH

* Bearish BOS

* Bearish OB Entered

* Bearish OB Exited

* New Bearish FVG

* Bullish FVG Mitigated

* New Bearish Opening Gap

* Bullish Opening Gap Mitigated

* New Bearish Volume Imbalance

* Bullish Volume Imbalance Mitigated

* Bearish Liquidity Grab

* Bullish Trendline Break

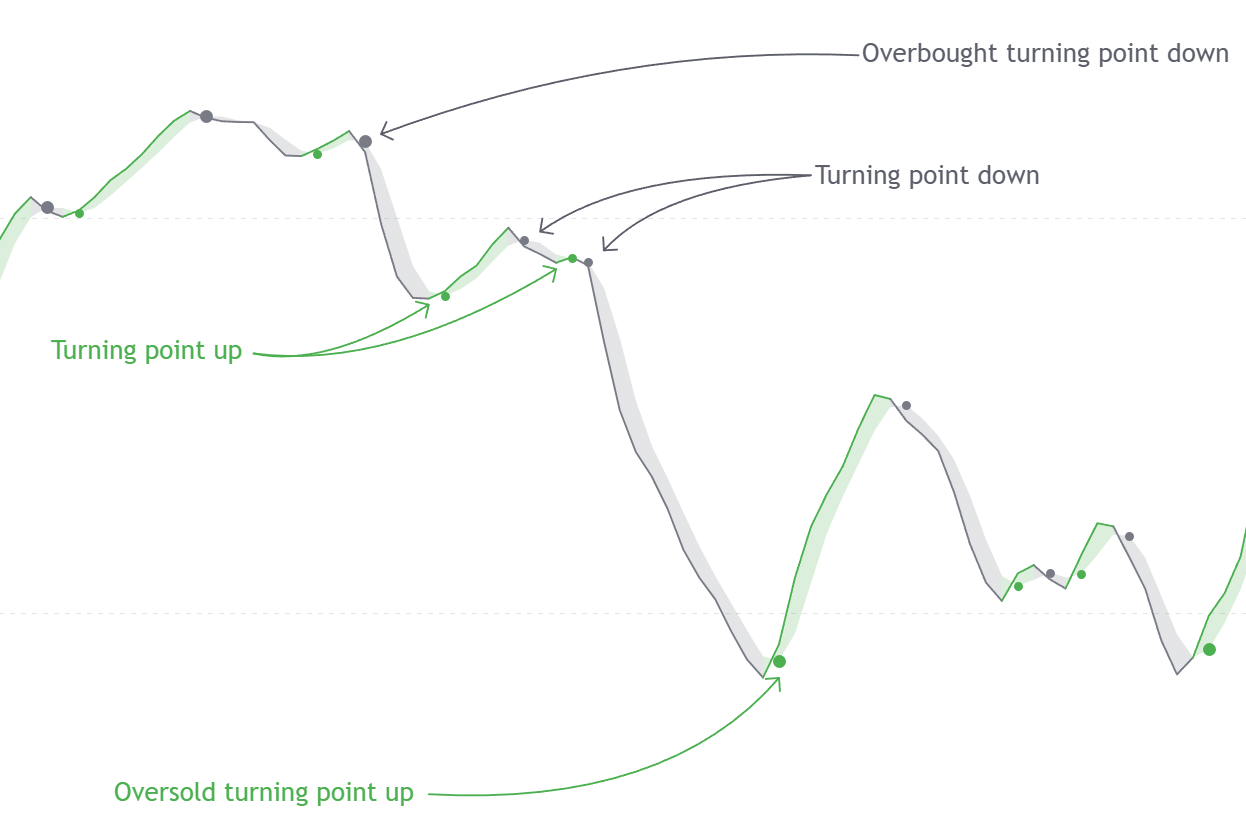

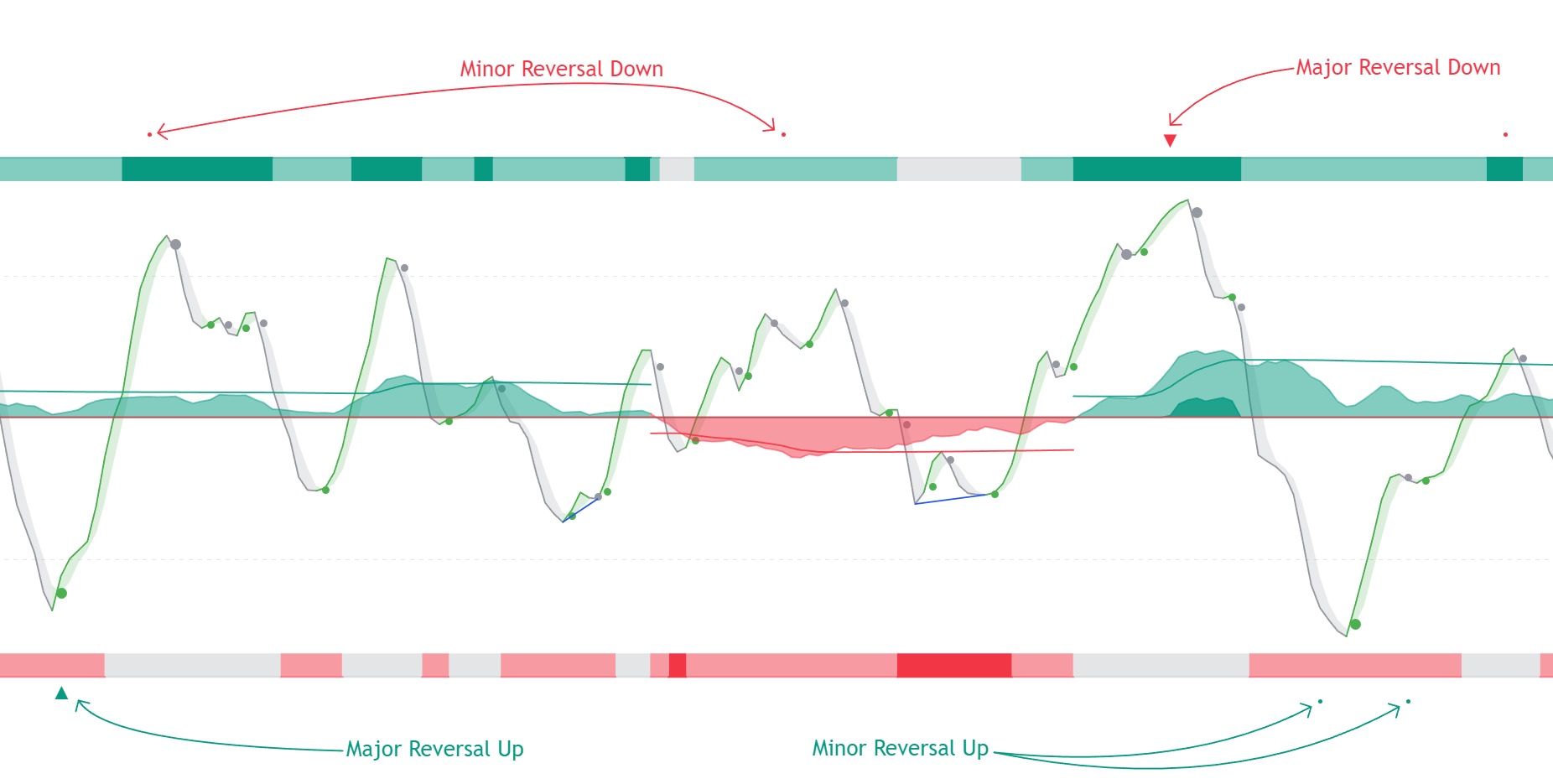

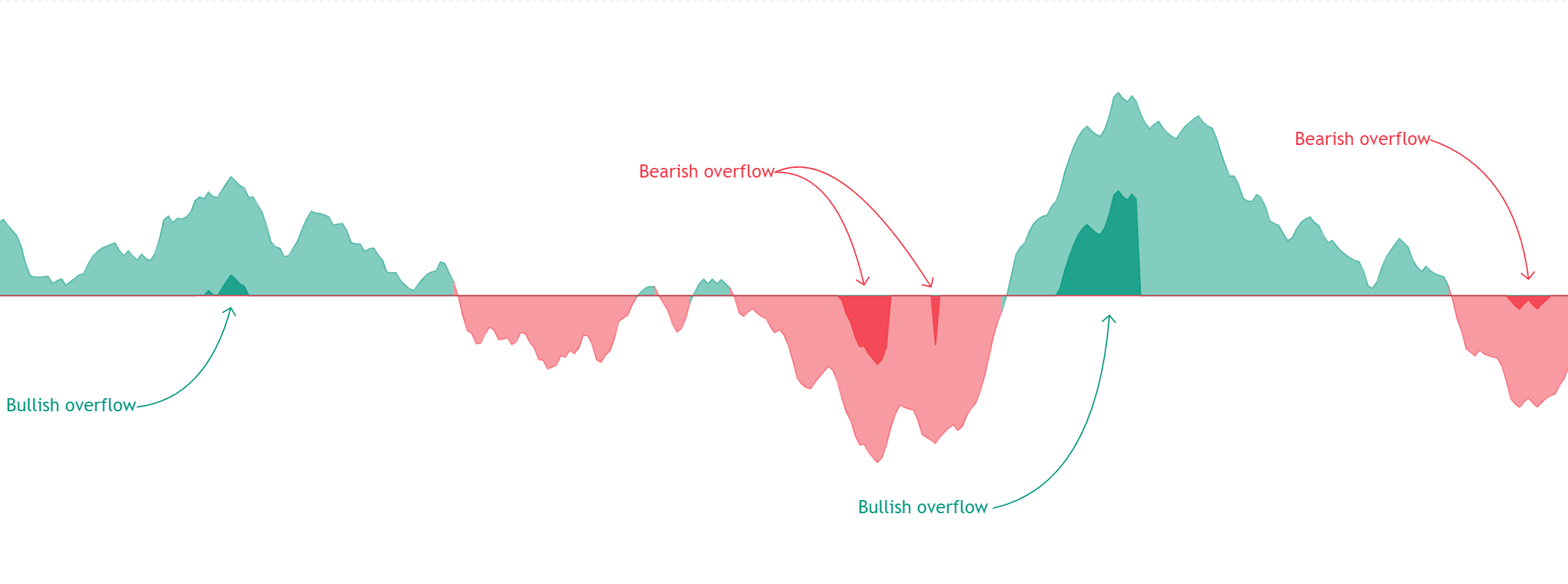

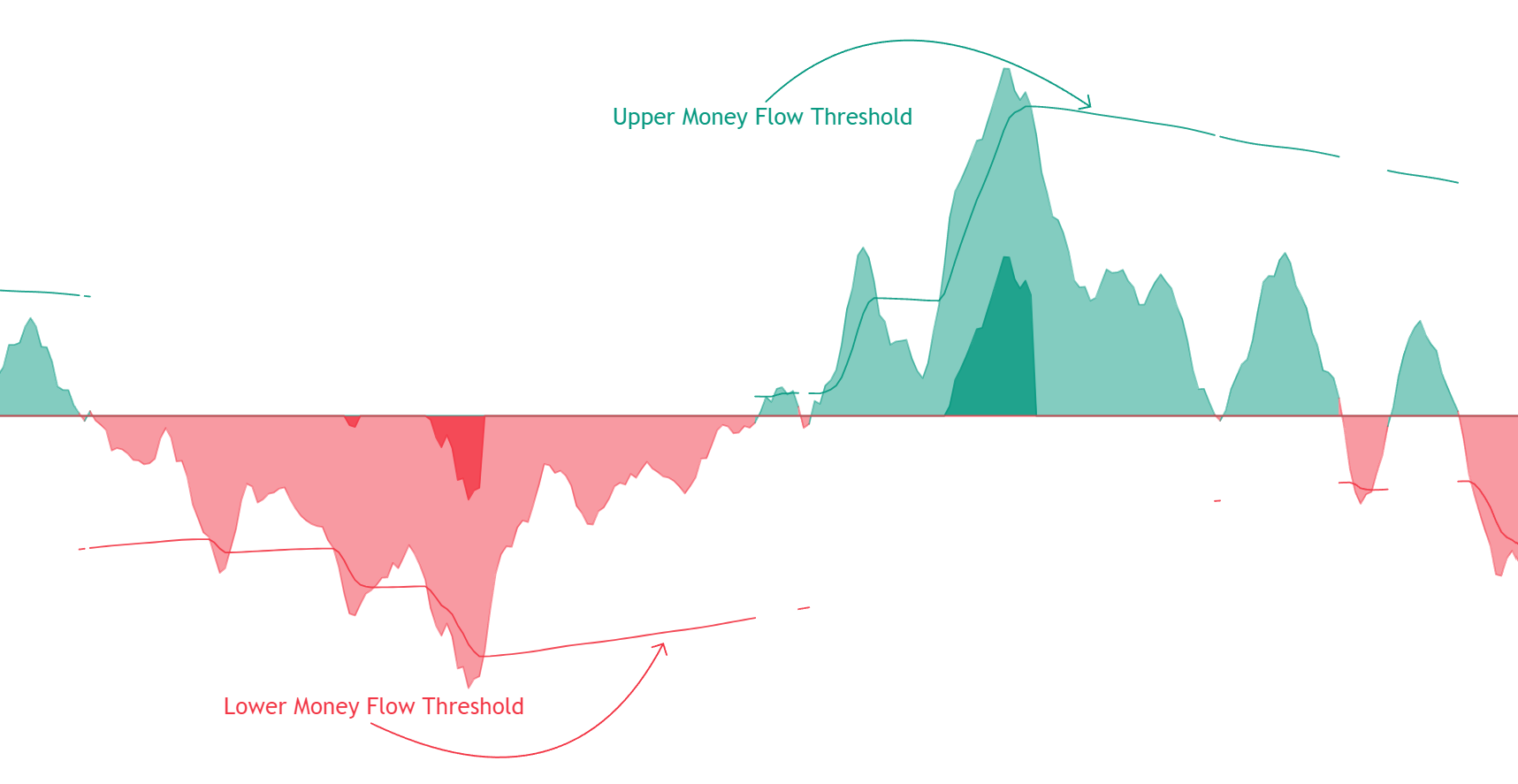

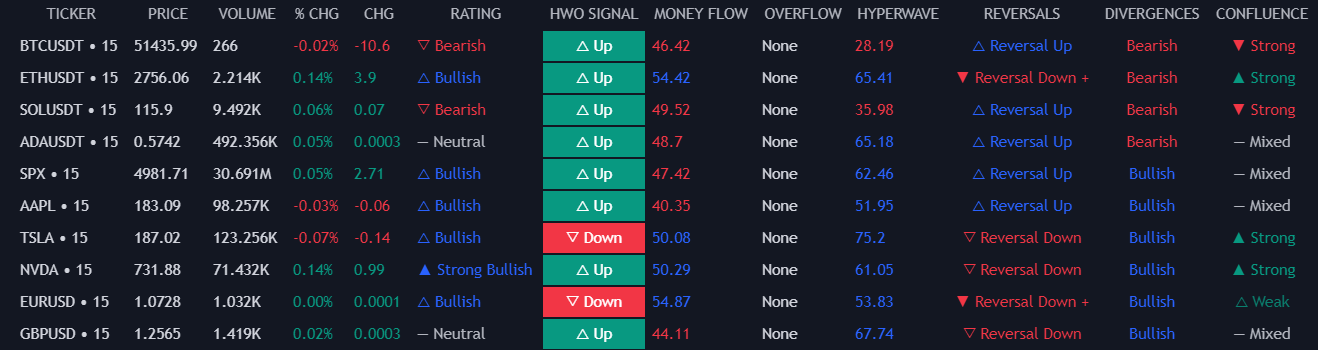

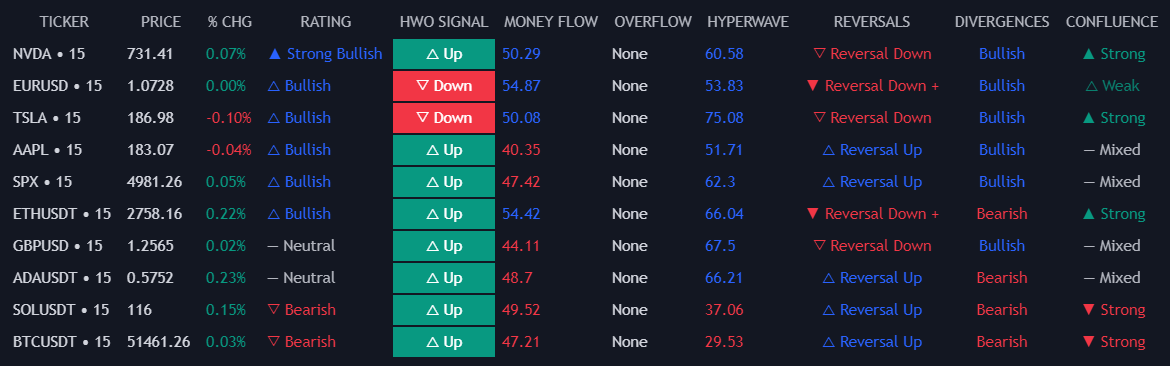

### Oscillator Matrix® Conditions [#oscillator-matrix-conditions]

***

#### Triggers [#triggers-2]

* New Bullish Overflow

* Money Flow Crossing Over 50

* HyperWave Oversold Bullish Signal

* HyperWave Crossing Over 80

* HyperWave Crossing Over 50

* Reversal Any Up

* New HyperWave Bullish Divergences

* New Bearish Overflow

* Money Flow Crossing Under 50

* HyperWave Overbought Bearish Signal

* HyperWave Crossing Under 20

* HyperWave Crossing Under 50

* Reversal Any Down

* New HyperWave Bearish Divergences

#### Filters [#filters-1]

* Bullish Overflow

* Money Flow Above 50

* HyperWave Above 80

* HyperWave Above 50

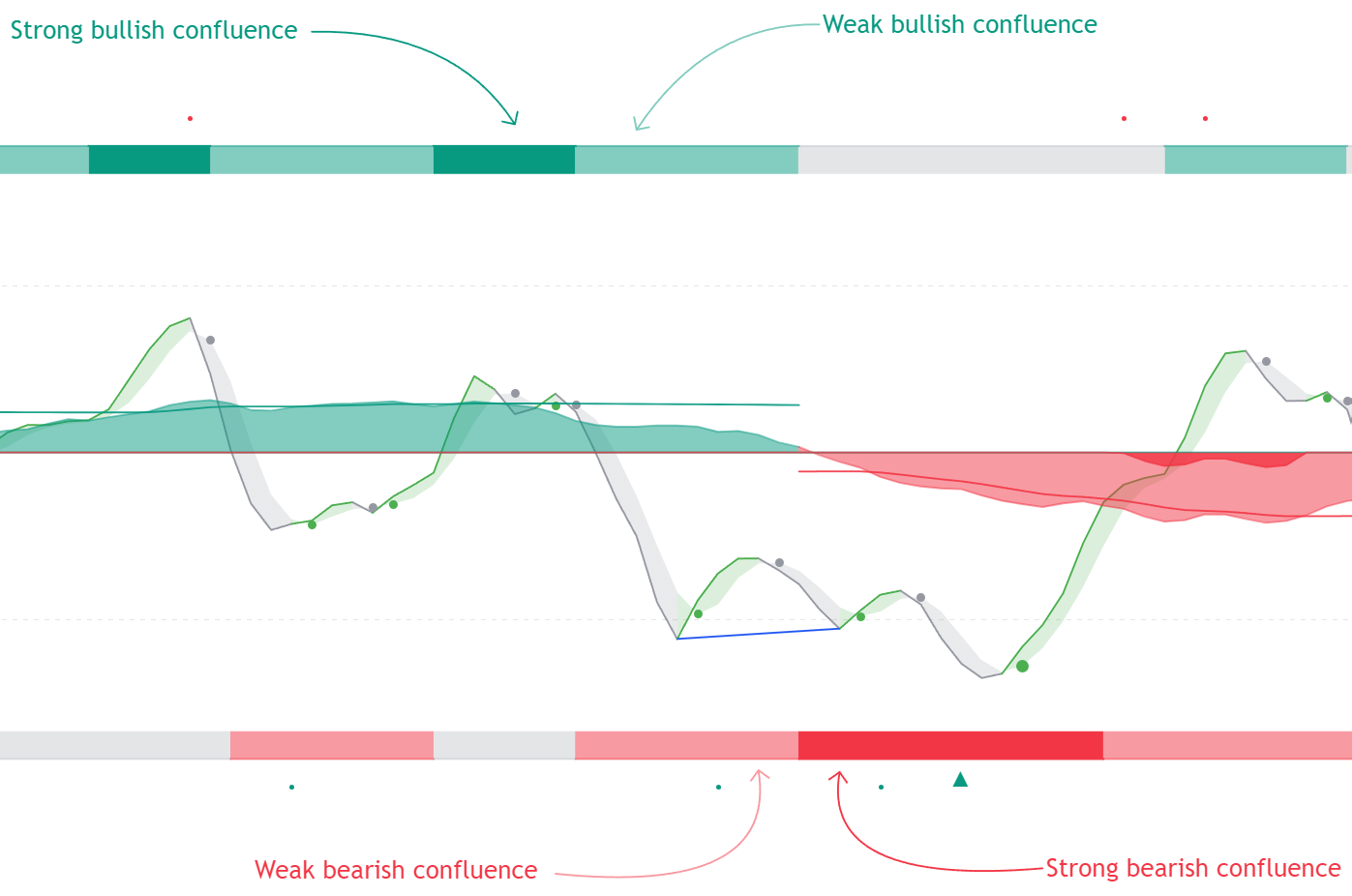

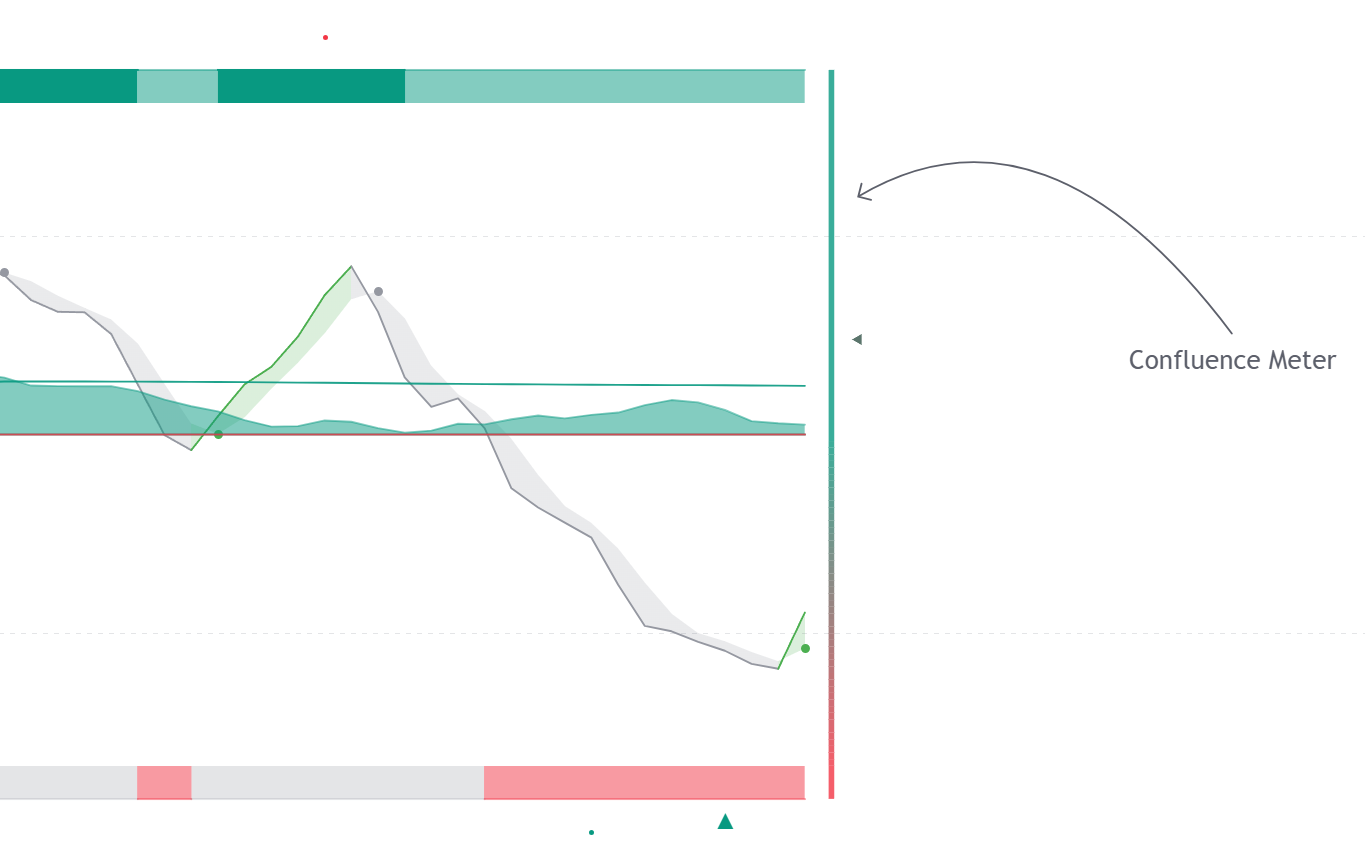

* Strong Bullish Confluence

* Weak Bullish Confluence

* Bearish Overflow

* Money Flow Below 50

* HyperWave Below 20

* HyperWave Below 50

* Strong Bearish Confluence

* Weak Bearish Confluence

## How To Fetch Strategies [#how-to-fetch-strategies]

Interacting with the AI Backtesting Assistant is straightforward. All users need to do is type a prompt in the chat box located at the bottom of their screen.

Here are examples of prompts that will trigger the AI Backtesting Assistant to retrieve a trading strategy:

* What is the best performing strategy across all crypto tickers on the 5-minute timeframe?

* Give me three strategies using fair value gaps that have a winrate above 80%.

* Find a strategy with above average net profit but below average drawdown.

Users can also click on one of the suggested prompts in the search group located above the input prompt.

The AI can access the following backtesting results for strategies:

* Net Profit

* Max Net Profit

* Closed Trades

* Winning Trades

* Losing Trades

* Winrate

* Gross Profit

* Gross Loss

* Profit Factor

* Max Drawdown

* Max Drawdown Percent

* Average Trade

* Average Winning Trade

* Average Losing Trade

Due to calculations being sensitive to data differences, our Drawdowns calculations are based on realized profits/losses, which is not the case on TradingView, this can explain why certain differences can be observed.

These results will be returned in a component in the chat.

If multiple strategies are returned, they will all be located within a table.

A maximum of 3 strategies can be returned in a table at once, while a maximum of three strategies can be returned from a single fetching operation.

If the AI needs to fetch more than 3 strategies it will fetch strategies sequentially.

The AI can also access to the following information from a strategy:

* Strategy begins at: When the strategy started being evaluated

* Strategy current position: Long, short, or flat if no positions are currently open

### Fetch Statistics Across The Entire Strategy Population [#fetch-statistics-across-the-entire-strategy-population]

The AI can get general statistics and data across the whole population of strategies it has access to.

Example of prompts doing this are:

* What is the total net profit of all bitcoin strategies you have?

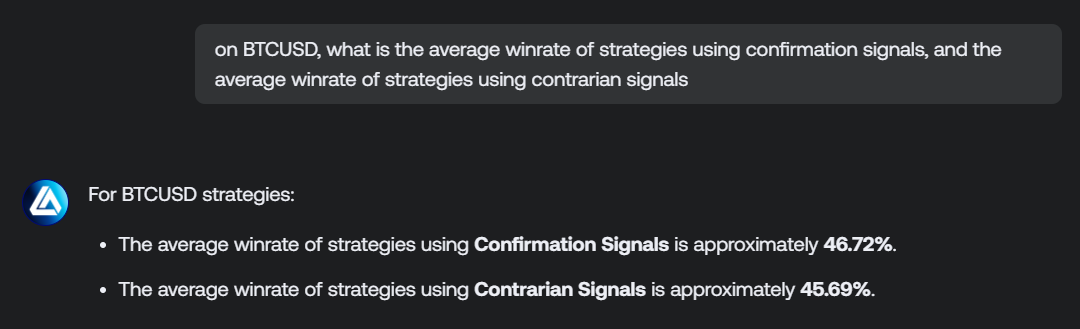

* On BTCUSD, are strategies using normal Confirmation signals better than the ones using strong Confirmation signals overall?

* What is total net profit of profitable strategies across stocks?

This can be useful to get big picture information about strategies.

Do note that such prompts can lead to high wait time for the results.

### Analyzing strategy trades [#analyzing-strategy-trades]

A returned strategy by the AI Backtesting Assistant contains a list of trades, each having information on its side (long / short), entry time and price, closing time and price, and P\&L result.

The AI Backtesting Assistant may filter trades by their index, trade side, result (win / loss), holding time (in minutes), P\&L, opening and closing time. Then an operation may be applied to a specific trade information from the filtered results.

Available capabilities from the trade analysis include:

* Trade filtering by index, trade side, result (win / loss), holding time (in minutes), P\&L, opening and closing time

* Operations on filtered subset such as average, median, count, sum, percentage

* Winning/Losing streak analysis

Example of typical questions one could ask related to trades of a strategy may include:

* Which trade has been the most/least profitable one?

* What is the entry and exit price price of most profitable long trade?

* What is the average trade duration of winning trades?

* What is the average profit/loss of trades with a duration above 50 minutes?

* How many winning trades occurred after 14 Jan 2025?

* What is the percentage of trades amongst the first 50 ones that are winning trades?

* What is the losing streak length before the last win?

* What is the average winning streak length?

* How many trades have a profit superior to the average winning trade?

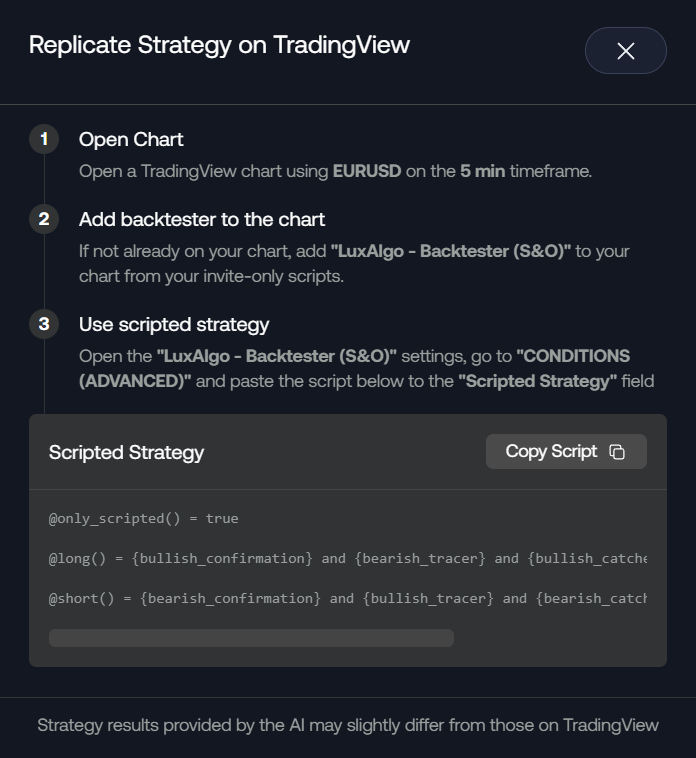

## Reproducing a Strategy on TradingView [#reproducing-a-strategy-on-tradingview]

Once you get a strategy you like, you may be inclined to add it to your chart to visualize it and further optimize its results on TradingView.

To do so, simply click on the TradingView logo located near the ticker symbol for the single strategy component, and to the right of a hovered row on a table containing strategies.

This will open a dialog box containing all the steps required to get the strategy on TradingView, as well as the scripted strategy which you must copy and paste to the relevant backtester.

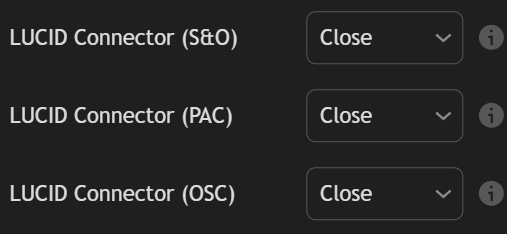

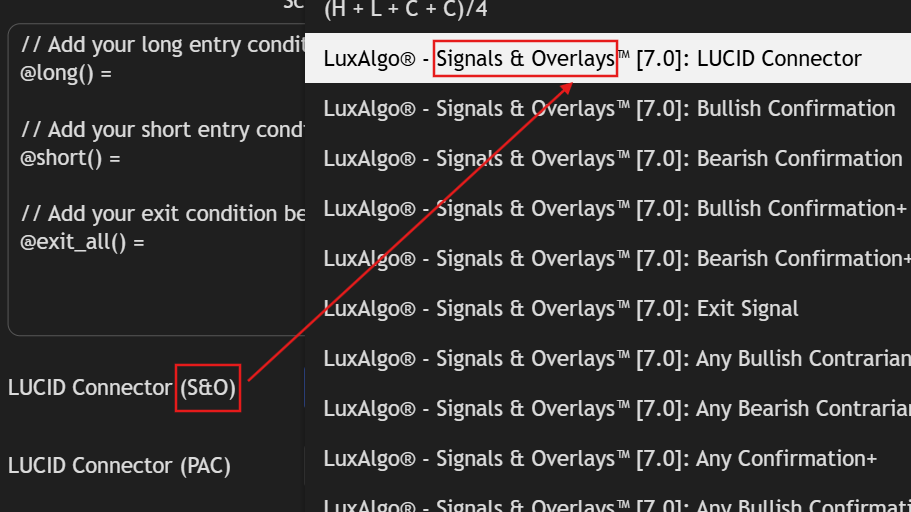

A strategy using multiple conditions from at least two toolkits will require using LUCID connectors, learn more about LUCID connectors [here](/docs/ai-backtesting/backtesters/strategy-scripting/lucid-connectors).

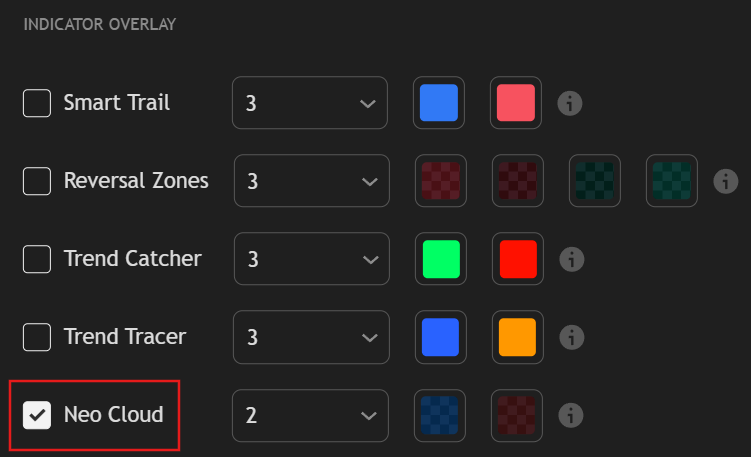

If replicating a strategy involves making use of LUCID conectors, **make sure you enable the relevant features**, for example, if a strategy using the **Trend Catcher** requires using the LUCID connector of the **Signals & Overlays** toolkit, make sure the Trend Catcher overlay is enabled in the toolkit settings.

We compute strategies using data that might different from the one on TradingView, which can limit the reproducibility of strategies returned by the AI.

Some users might not be able to reproduce exact strategy results due to the limitation on how much data certain users can access.

## Saving Strategies [#saving-strategies]

Strategies can be saved in the sidebar by clicking on the star icon located near the ticker symbol for the single strategy component, and to the right of a hovered row on a table containing strategies.

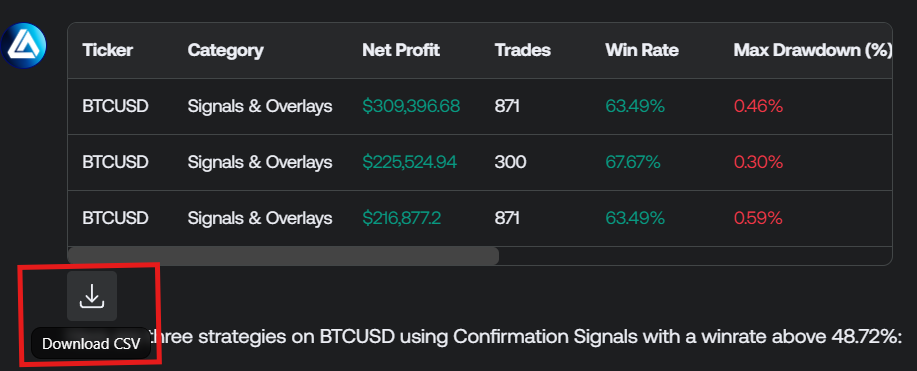

Additionally, strategies returned in a table can be exported as a CSV file.

## Prompting Tips [#prompting-tips]

The AI can make mistakes when fetching strategies, as this is a very complex process depending on the user query.

We will always aim to improve the AI Backtesting Assistant over time; however, the following tips can help you get the most from our AI.

### Make Detailed Queries [#make-detailed-queries]

Make sure to detail every aspect of the strategy you want to fetch if you have a precise one in mind, for example:

| Original | Improved |

| ------------------------------------------------------------ | ---------------------------------------------------------------------------------------------------------------------------- |

| Fetch a strategy that uses Confirmation Signals | Fetch a strategy that only uses Confirmation Signals and no other conditions |

| I want a PAC strategy that goes long on a new FVG, and CHoCH | I want a PAC strategy that goes long when:

- Step 1: a new bullish FVG occur - Step 2: a bullish CHoCH occur |

| I want the best strategy | I want the strategy with the highest net profit on BTCUSD 5 minute |

Context and details will help the AI avoid making guesses about your query.

### Encourage the AI to Improve [#encourage-the-ai-to-improve]

The AI Backtesting Assistant can be fairly self-aware if a fetched strategy doesn't meet a user criteria, and will then retry.

But if the AI response is clearly mistaken, then it can be good to let it know using a prompt encouraging re-evaluation of the fetching process:

> The strategy your returned is not the one I want. Correct the issue in your fetching process and retry to fetch the strategy in accordance with my query.

### Split Complex Queries Into Multiple Tasks [#split-complex-queries-into-multiple-tasks]

The AI will be more prone to mistakes if the query is complex, as such, it is best to do follow-up messages asking about the details of a strategy rather than asking the AI to give those alongside other information.

For example:

> Return a good strategy on BTCUSD, alongside the average net profit of all strategies on BTCUSD that use Confirmation signals, then tell me what the highest winrate strategy is, using the same conditions as the first one

The AI Backtesting Assistant might provide more relevant answers if we let context accumulate by splitting and re-ordering our initial query into multiple ones:

Return a good strategy on BTCUSD

Find the strategy with the highest winrate that use the same exact entry conditions returned previously

Return the average net profit of all strategies on BTCUSD that use Confirmation Signals.

# Introduction (/docs/ai-backtesting/introduction)

Access the AI Backtesting Assistant here.

The [AI Backtesting Assistant](https://www.luxalgo.com/backtesting/chat/) is a conversational AI leveraging a variety of state of the arts large language models to scan and retrieve a wide variety of strategies built using core features from our Signals & Overlays®, Price Action Concepts®, and Oscillator Matrix® toolkits. It also can give contextual information about our products & markets.

The AI Backtesting Assistant is only available for Ultimate users.

To learn more about the capabilities of the AI Backtesting Assistant, see the pages below:

Fetch strategies simply by using natural language

View detailed strategies backtset results

Learn more about LuxAlgo toolkits using our assistant

Common issues and solutions

## FAQ [#faq]

All users can access AI Backtesting [here](https://www.luxalgo.com/chat). Users with Premium and Ultimate plans can benefit from higher usage limits.

Credits is the currency system used to control the usage amount a user has with our AI products. The credit balance of an user is shared across both AI Backtesting platform and Quant, our Pine Script® coding agent.

User credits reset every first of the month.

The AI Backtesting Assistant has access to the backtesting results of over 10 million trading strategies using core features from the Signals & Overlays®, Price Action Concepts®, and Oscillator Matrix® toolkits.

Strategies are evaluated for some of the most traded tickers across 3 timeframes: 5 minute, 15 minute, and 1 hour.

**Included ticker symbols by market:**

* AAPL

* AMD

* AMZN

* BABA

* CELH

* COIN

* CRWD

* DIS

* DUOL

* GME

* GOOG

* HOOD

* INTC

* MA

* META

* MSFT

* MSTR

* NFLX

* NKE

* NVDA

* ORCL

* PLTR

* PYPL

* RIVN

* SMCI

* SNOW

* SOFI

* TSLA

* UBER

* WMT

* ARKK

* IWM

* QQQ

* SPY

* VTI

* AAVEUSDT (Binance)

* ADAUSDT (Binance)

* ATOMUSDT (Binance)

* AVAXUSDT (Binance)

* BCHUSDT (Binance)

* BNBUSDT (Binance)

* BTCUSDT (Binance)

* DOGEUSDT (Binance)

* DOTUSDT (Binance)

* EOSUSDT (Binance)

* ETHUSDT (Binance)

* HBARUSDT (Binance)

* HYPEUSDT (Kucoin)

* JUPUSDT (Binance)

* KASUSDT (Kucoin)

* LINKUSDT (Binance)

* LTCUSDT (Binance)

* SHIBUSDT (Binance)

* POLUSDT (Binance)

* SOLUSDT (Binance)

* SUIUSDT (Binance)

* TONUSDT (Binance)

* TRXUSDT (Binance)

* UNIUSDT (Binance)

* VETUSDT (Binance)

* XLMUSDT (Binance)

* XRPUSDT (Binance)

* AUDJPY

* AUDUSD

* EURAUD

* EURGBP

* EURUSD

* EURJPY

* GBPAUD

* GBPJPY

* GBPUSD

* NZDUSD

* USDCAD

* USDCHF

* USDJPY

* XAGUSD

* XAUUSD

* UKOIL

* NQ

* ES

* RTY

* YM

* GC

* SI

* CL

* NG

* PL

* ZC

* ZW

* ZS

* 6E

* 6J

US equities (Stocks and ETFs) use regular trading hours and are based on the Cboe BZX exchange.

Futures are based on continuous contracts and use electronic trading hours, without adjustment for contracts changes. Contract roll is performed taking into account a combination of volume and openinterest.

Unlike TradingView, Futures contracts roll on the day prior to expiration.

Yes, users have a token balance that determines how much they can use the AI, however, it is highly unlikely you will ever reach the end of your token balance. It resets at the first of each month and once it reaches 0, the AI will no longer be available until the balance is refreshed.

Yes, strategy results provided by the AI can be exported as a CSV file for easy access and analysis.

Backtests are performed on all the tickers on Monday, Wednesday, and Friday at 23:30 UTC, using our own internal system on data from quality third party providers, ensuring users can reproduce the results given by the AI on TradingView if needed.

Strategies starts being evaluated at a specific date, which can be returned by the AI assistant.

No, currently backtests are performed on Monday, Wednesday, and Friday at 23:30 UTC for all strategies. As a result you might potentially see some more recent trades once you replicate a given strategy on TradingView.

We are actively working on updating strategies continuously.

Due to the potential difference in market data and processes it is possible for backtest results to slightly differ from what you might observe on TradingView.

## Disclaimer [#disclaimer]

This AI tool’s backtesting data & analytics are for informational purposes only and do not constitute financial advice or recommendations to buy or sell any financial product, including but not limited to securities, derivatives, cryptocurrencies, or other investment instruments.

This tool may contain errors, and past performance is not indicative of future results. Always conduct your own research and consult with a professional financial advisor.

LuxAlgo is not liable for any decisions made based on any information given. Read our [full disclaimer](https://www.luxalgo.com/legal/disclaimer/).

# Troubleshooting (/docs/ai-backtesting/troubleshooting)

The AI Backtesting Assistant is an early feature, and such might face several limitations described in this page.

Don't hesitate to send your feedback at [support@luxalgo.com](mailto:support@luxalgo.com) or in our [Discord server](https://discord.com/invite/LUX).

## I can't use the AI Backtesting Assistant [#i-cant-use-the-ai-backtesting-assistant]

The AI Backtesting assistant is only available for our Ultimate users. Users without a plan can purchase one [here](https://www.luxalgo.com/pricing/).

Users subscribed to the Premium plan will need to upgrade to the Ultimate plan to use the AI Backtesting Assistant.

## The AI is not responding to my message [#the-ai-is-not-responding-to-my-message]

To ensure fair and consistent access to the AI Backtesting Assistant, users are subject to rate limits defined in terms of concurrent requests.

If the maximum number of concurrent requests is exceeded, messages sent to the AI Backtesting Assistant will take longer to get answered.

Waiting for some time will generally resolve the issue.

## Reached maximum monthly usage for the AI Backtesting Assistant [#reached-maximum-monthly-usage-for-the-ai-backtesting-assistant]

Because of the amount of compute necessary to run our LLM and to prevent potential abuse, users have a limited usage of the AI Backtesting Assistant.

The amount of usage is determined by the amount of content returned by the AI, as such large messages can consume more usage than more frequent small messages.

The monthly usage is reset every first of the month.

In order to significantly save on usage you can refresh the page to clear the chat, as generating new messages on large conversations will drain usage more quickly.

You can also use a cheaper model to reduce usage, the cost of a model is indicated by the amount of $ signs present in the model selection.

## I am seeing very different strategy results on Tradingview [#i-am-seeing-very-different-strategy-results-on-tradingview]

We compute strategies using data that might be slightly different on TradingView.

The amount of data you have access to can also affect its ability to reproduce strategies, as strategies are backtested using 20.000 bars.

## Specific models do not work [#specific-models-do-not-work]

Some models can be subject to geo-restriction and as such might not be usable by specific users.

We always include one model that is not subject to this restriction, such as Qwen models.

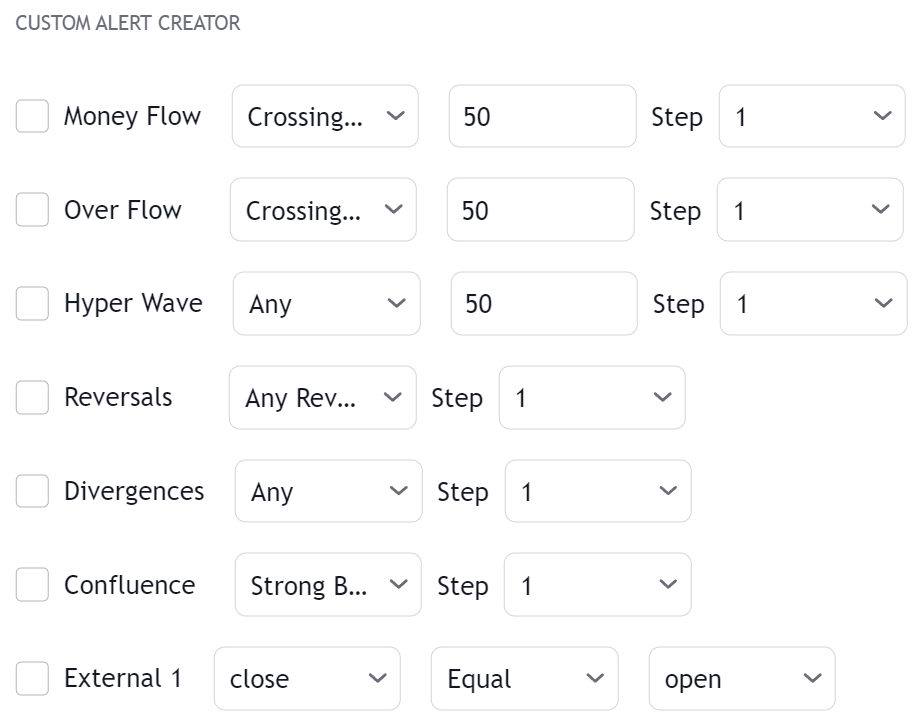

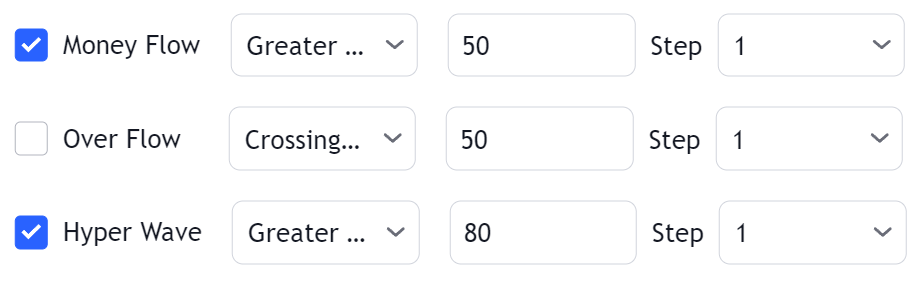

# Creating Alerts (/docs/ai-strategy-alerts/creating-alerts)

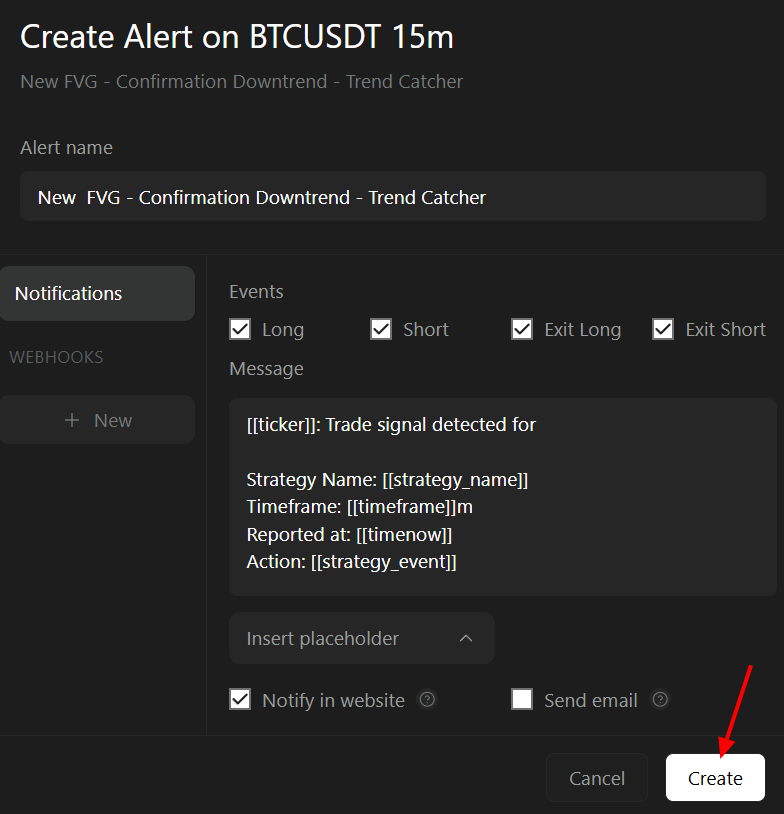

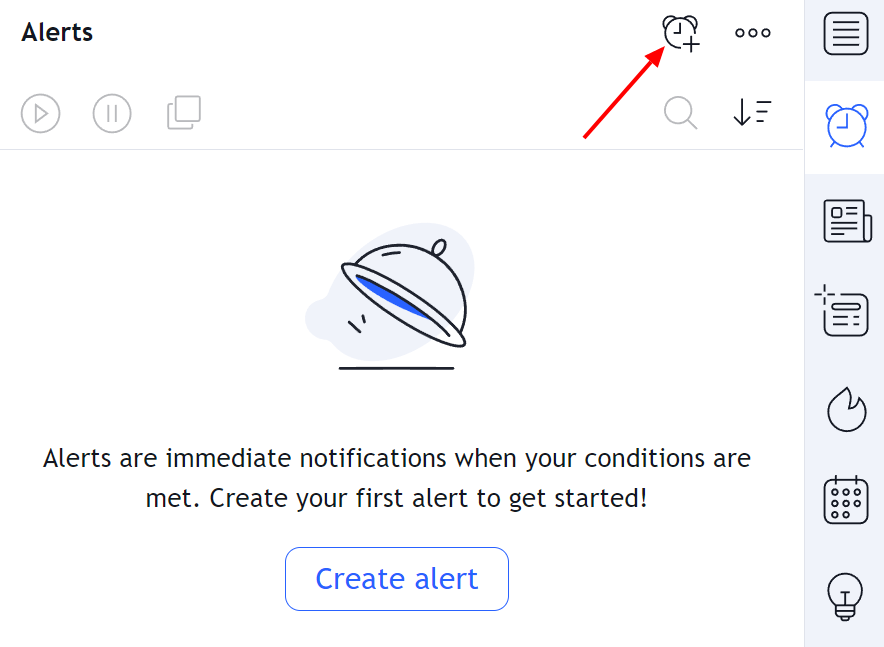

Users can easily create alerts from strategies by requesting them to our [AI Assistant](/docs/ai-backtesting/introduction).

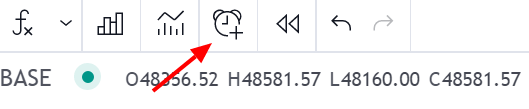

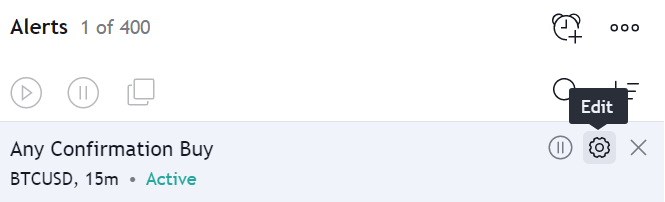

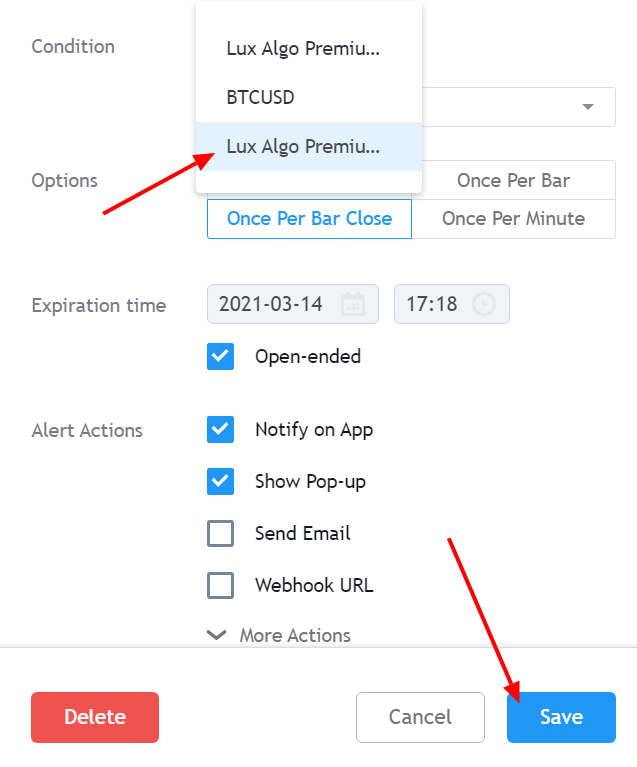

Once a strategy is fetched the user can create an alert from it by clicking on the alarm icon. This will open up a menu allowing to customize the alert. Once done the user can create the alert by clicking on the button "Create".

Alerts can also be created from saved strategies in the sidebar.

Users can have a maximum of 100 alerts running.

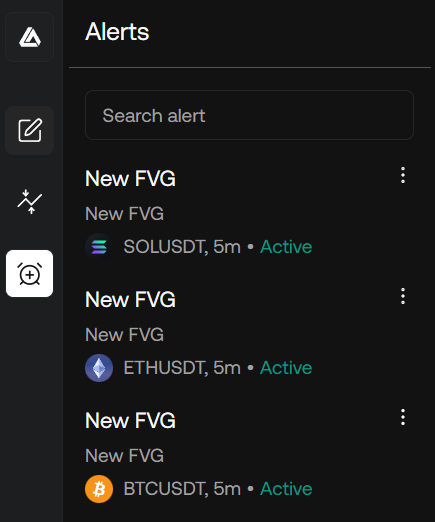

## Accessing Created Alerts [#accessing-created-alerts]

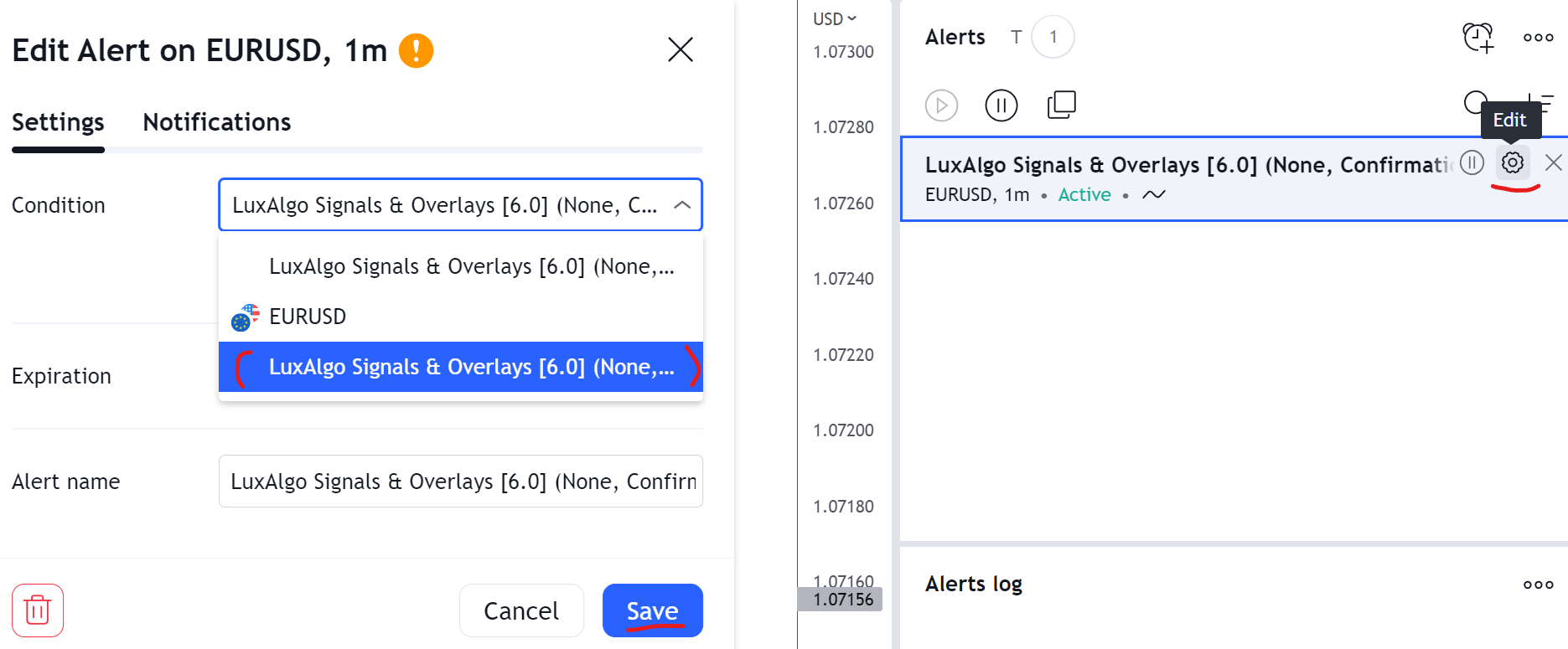

Created alerts can be accessed from the sidebar. From there the user can edit, pause, or delete them.

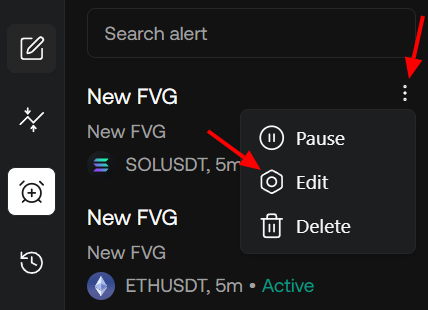

### Editing Created Alerts [#editing-created-alerts]

Alerts can be edited at any time by clicking on the kebab menu in the sidebar. Once edited and saved, the alert will use the new user-set configuration for future alerts.

# Introduction (/docs/ai-strategy-alerts/introduction)

Strategy alerts within our AI platform are only available to our Ultimate users. [Upgrade](https://www.luxalgo.com/pricing) your subscription to start creating strategies & alerts.

Any AI trading strategy you create out of millions on the LuxAlgo platform can now generate advanced alerts. This feature sends alerts triggered by events such as going long, short, exits, taken by the strategies available from using our [AI Assistant](/docs/ai-backtesting/introduction).

LuxAlgo users may use our alerts system to receive notifications in the form of in app notifications within our app, emails, or make use of our integrated webhooks for more advanced usage through third party platforms such as automated trading.

## Features [#features]

## FAQ [#faq]

See [this guide](/docs/ai-strategy-alerts/creating-alerts).

Only users with an **Ultimate** subscription may create alerts.

Users with an **Ultimate** subscription are limited to 100 alerts.

Yes, users can enable emails to be sent when an alert triggers.

Currently alerts are limited to the supported tickers and timeframes, as well as the available strategies in our database.

Yes, we allow creating up to 4 webhooks for a single alert.

Yes, it is possible to use our webhooks to integrate with third party automation platforms to place orders.

We do not guarantee the proper execution of orders nor the arrival of requests to set webhooks.

Yes, it is possible for alerts to be delayed depending on the load on our systems and other external factors.

No, alerts created from strategies on futures use a real-time data feed.

Canceling or downgrading your Ultimate subscription will keep your existing alerts active. You will be able to create alerts only until the end of the subscription.

Once your Ultimate subscription ends, all your alerts will be stopped.

If you pause your subscription, all of your alerts will stop immediately.

All alerts will be immediately stopped but will remain tied to your account in the state they were set as.

If you resubscribe, you will regain access to previously created alert and may reactivate them.

## Disclaimer [#disclaimer]

Alerts and notifications provided by LuxAlgo are intended **for informational and display purposes only**. They are **not designed or guaranteed for trading execution, investment decisions, or financial advice**.

LuxAlgo does not guarantee the **availability, accuracy, reliability, or timely delivery** of any alerts, notifications, or webhooks. **Downtime or delivery failures may occur** at any time without prior notice.

By using LuxAlgo alerts, you acknowledge that LuxAlgo **is not liable for any losses, damages, or outcomes** resulting from the use, interpretation, or reliance upon such alerts, notifications, or webhooks.

Read our [full disclaimer](https://www.luxalgo.com/legal/disclaimer/).

# Notifications (/docs/ai-strategy-alerts/notifications)

Users can be notified of triggered alerts via in-app notifications and/or emails.

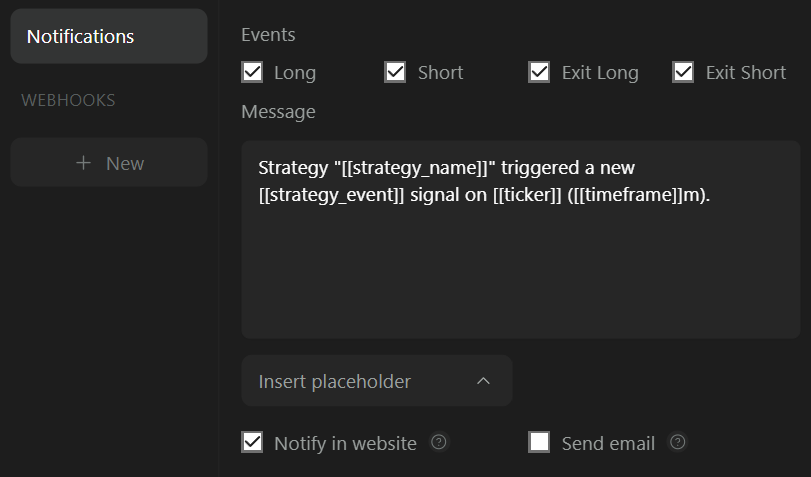

The default view when creating or editing an alert displays the notification settings by default and can be accessed at any time by clicking on "Notifications" in the alert menu sidebar.

## Events [#events]

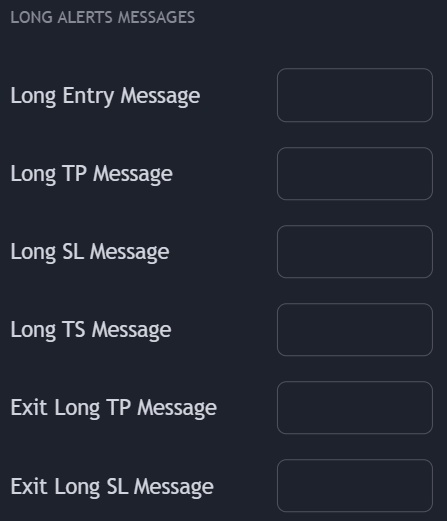

The event toggles determine which strategy events (long, short, exit long, exit short) trigger an in-app or email notification (if enabled).

## Alert message [#alert-message]

The alert message field determines the content that appears in the in-app notification or email.

### Placeholders [#placeholders]

Users might want to include dynamic data in their alert message, such as which strategy event triggered the alert or the strategy's entry price.

This is possible using placeholders. The syntax is `[[placeholder_name]]`. The following placeholders are available.

| Placeholder | Description | |

| -------------------------------- | ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------ | ---------- |

| \[\[currency]] | Currency of the asset the strategy is based on | |

| \[\[current\_contract\_myy]] | For strategies set on futures, current contract traded by the strategy in the format `[ROOT][MONTH_CODE][2 digit YEAR]`, for example `ESZ25` | `string` |

| \[\[current\_contract\_myyyy]] | For strategies set on futures, current contract traded by the strategy in the format `[ROOT][MONTH_CODE][4 digit YEAR]`, for example `ESZ2025` | `string` |

| \[\[exchange]] | Exchange where the asset is traded | |

| \[\[strategy\_event]] | Event originating from the strategy, options include "long", "short", "exit long", "exit short" | |

| \[\[strategy\_id]] | A unique identifier associated to the strategy | |

| \[\[strategy\_market\_position]] | Current position of the strategy, options include "long", "short", "flat" | |

| \[\[strategy\_name]] | Name of the strategy | |

| \[\[strategy\_order\_action]] | Action taken by the strategy, options include "buy" and "sell". For this placeholder an exit long would lead to the value being "sell" while an exit short would lead to "buy" | |

| \[\[strategy\_order\_price]] | Price at which the order was executed | |

| \[\[ticker]] | Ticker symbol the strategy is based on | |

| \[\[time]] | ISO 8601 datetime (including milliseconds) of the opening time of the candle for which the strategy event occurred. Example `2025-11-17T23:14:52.123Z` | `datetime` |

| \[\[timeframe]] | Timeframe the strategy is based on | `number` |

| \[\[timenow]] | ISO 8601 datetime (including milliseconds) of the alert being triggered. Example `2025-11-17T23:14:52.123Z` | `datetime` |

Example of a strategy alert message using placeholders:

```

Strategy "[[strategy_name]]" triggered a new [[strategy_event]] signal on [[ticker]] ([[timeframe]]m) at price [[strategy_order_price]].

```

Placeholders may be inserted in the message directly through the "Placeholders" dropdown; click a placeholder to insert it.

## In-App Notifications [#in-app-notifications]

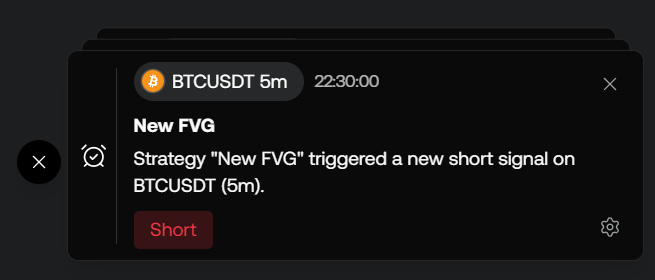

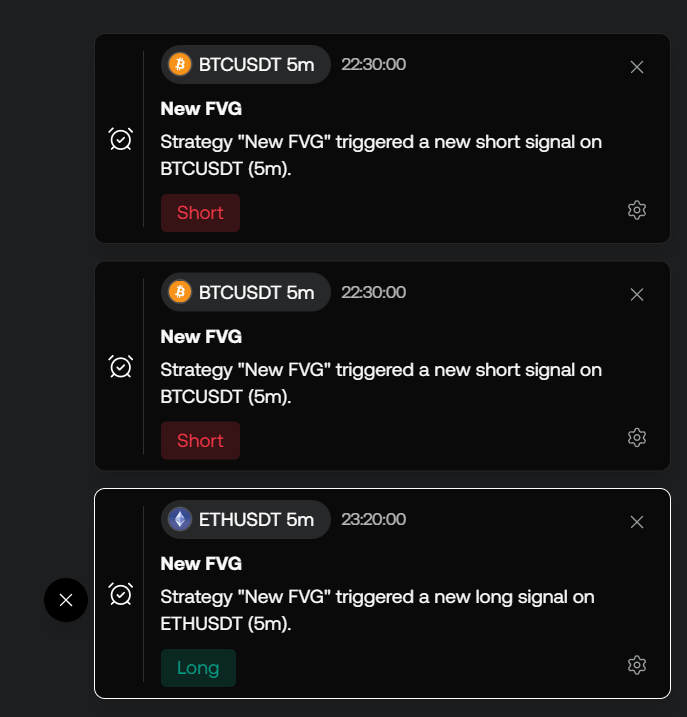

In-app notifications display small cards indicating an alert has been triggered. On desktop, they appear at the bottom-right of the screen; on mobile, at the bottom.

Hovering over a card shows messages from older alerts. Removing a card displays the next oldest alert (if any) at the top of the list.

Users can edit alerts directly from the cards by clicking the gear icon in the bottom-right.

## Emails [#emails]

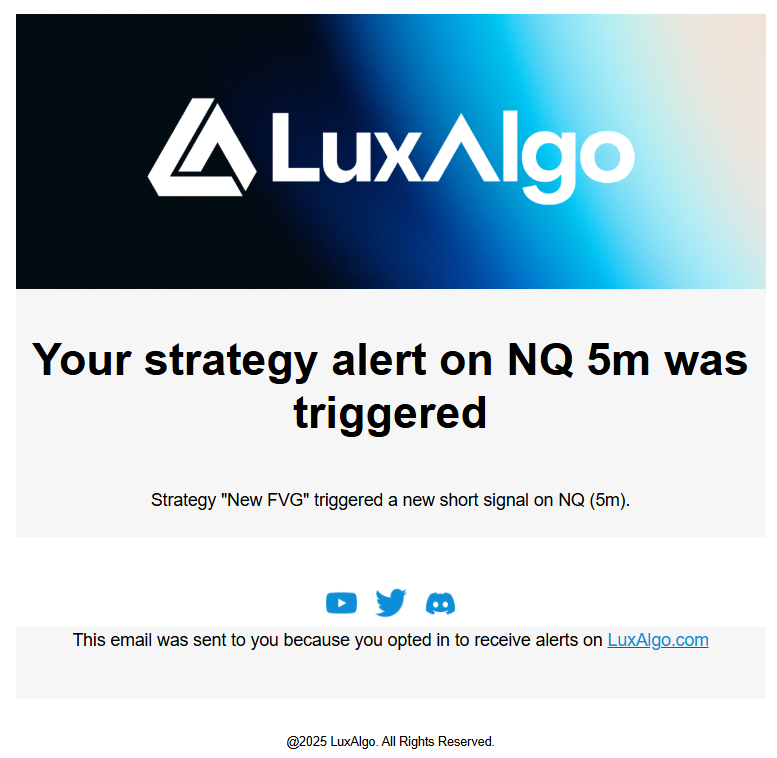

When a strategy alert is triggered, the user can receive an email at the address associated with their account.

To receive emails, enable "Send email" in the Notifications settings at the bottom-right.

# Webhooks (/docs/ai-strategy-alerts/webhooks)

Webhooks allow strategy alerts to be sent to third-party applications such as Discord, Telegram, automation platforms, or anywhere for advanced usage such as automated trading.

## Creating a webhook [#creating-a-webhook]

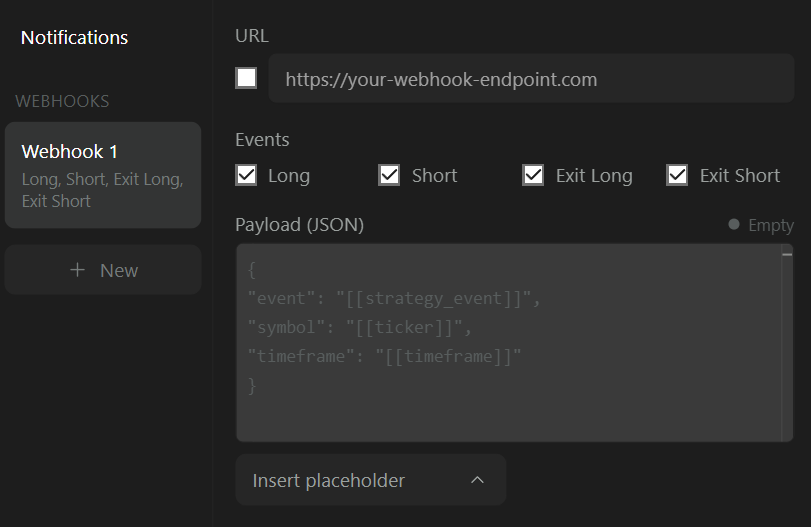

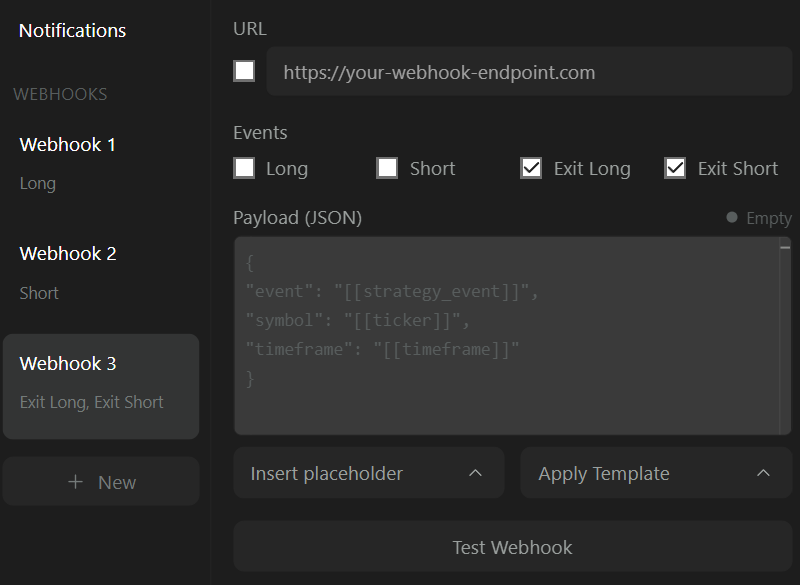

To create a webhook, simply look at the alert menu sidebar and click `+ New` under the **WEBHOOKS** section. This will open the settings for the new webhook, which will also appear in the alert menu sidebar.

Users can create up to 4 webhooks.

## Webhook Settings [#webhook-settings]

***

### Webhook URL (Required) [#webhook-url-required]

The URL of the webhook that will be reached when an alert is triggered. Only valid URLs are allowed.

Once a valid URL is entered, the webhook toggle can be enabled.

### Events [#events]

The event toggles determine for which strategy events (long, short, exit long, exit short) a webhook is triggered.

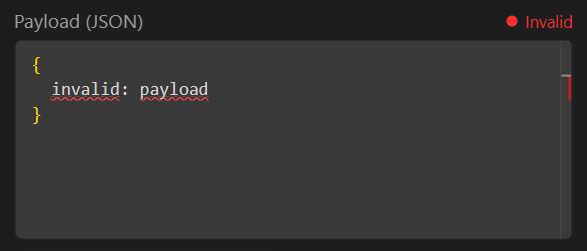

### Payload (Optional) [#payload-optional]

The payload field should contain the data sent to the webhook. The expected format for the payload is JSON.

> Learn more about the JSON format [here](https://www.geeksforgeeks.org/javascript/json-introduction).

If the payload is invalid it will be indicated.

If no payload is provided an empty JSON `{}` will be sent.

#### Placeholders [#placeholders]

Users might want to include in their alert message dynamic data, such as which strategy event triggered the alert or the entry price of the strategy.

This is possible by using placeholders. The placeholder syntax is as follows `[[placeholder_name]]`. The following placeholders are available.

| Placeholder | Description | Type |

| -------------------------------- | ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------ | ---------- |

| \[\[currency]] | Currency of the asset the strategy is based on | `string` |

| \[\[current\_contract\_myy]] | For strategies set on futures, current contract traded by the strategy in the format `[ROOT][MONTH_CODE][2 digit YEAR]`, for example `ESZ25` | `string` |

| \[\[current\_contract\_myyyy]] | For strategies set on futures, current contract traded by the strategy in the format `[ROOT][MONTH_CODE][4 digit YEAR]`, for example `ESZ2025` | `string` |

| \[\[exchange]] | Exchange where the asset is traded | `string` |

| \[\[strategy\_event]] | Event originating by the strategy, options include "long", "short", "exit long", "exit short" | `string` |

| \[\[strategy\_id]] | A unique identifier associated to the strategy | `string` |

| \[\[strategy\_market\_position]] | Current position of the strategy, options include "long", "short", "flat" | `string` |

| \[\[strategy\_name]] | Name of the strategy | `string` |

| \[\[strategy\_order\_action]] | Action taken by the strategy, options include "buy" and "sell". For this placeholder an exit long would lead to the value being "sell" while an exit short would lead to "buy" | `string` |

| \[\[strategy\_order\_price]] | Price at which the order was executed | `number` |

| \[\[ticker]] | Ticker symbol the strategy is based on | `string` |

| \[\[time]] | ISO 8601 datetime (including milliseconds) of the opening time of the candle for which the strategy event occurred. Example `2025-11-17T23:14:52.123Z` | `datetime` |

| \[\[timeframe]] | Timeframe the strategy is based on | `number` |

| \[\[timenow]] | ISO 8601 datetime (including milliseconds) of the alert being triggered. Example `2025-11-17T23:14:52.123Z` | `datetime` |

Even though the result of a placeholder can have a specific type, we only consider placeholders valid if they are strings (in between double quotation marks) in the payload.

Example of valid payload:

```json

{

"id": "my_unique_id",

"time": "[[timenow]]",

"event": "[[strategy_event]]",

"year": 2025,

"strategy conditions":

{

"long": "Confirmation Any Bullish",

"short": "Confirmation Any Bearish"

}

}

```

Placeholders may be inserted in the message directly through the "Placeholders" dropdown and clicking in the specific placeholder to insert. These will be inserted as a string directly.

## Creating Multiple Webhooks [#creating-multiple-webhooks]

Users can create up to 4 webhooks, one for different events, different URLs, or payloads.

This is useful if the URL or expected payload for specific events are different, or if a specific alert should be delivered to multiple platforms at the same time.

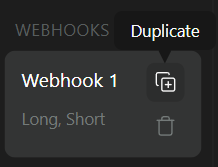

### Duplicating Webhooks [#duplicating-webhooks]

To easily preserve fields such as webhook URL and payload, users can duplicate the webhook by hovering on its corresponding item in the alert menu sidebar, clicking on the duplicate button will duplicate the webhook.

Duplicated webhooks come with the webhook URL toggle disabled.

## Templates [#templates]

Alerts and notifications provided by LuxAlgo are intended **for informational and display purposes only**. They are **not designed or guaranteed for trading execution, investment decisions, or financial advice**.

LuxAlgo does not guarantee the **availability, accuracy, reliability, or timely delivery** of any alerts, notifications, or webhooks. **Downtime or delivery failures may occur** at any time without prior notice.

By using LuxAlgo alerts, you acknowledge that LuxAlgo **is not liable for any losses, damages, or outcomes** resulting from the use, interpretation, or reliance upon such alerts, notifications, or webhooks.

Read our [full disclaimer](https://www.luxalgo.com/legal/disclaimer/).

### TradersPost [#traderspost]

Create a new strategy on TradersPost, once created navigate to it, click on "Webhook" and copy the provided URL.

In the LuxAlgo strategy alert creation menu create a new webhook, add the provided webhook URL, and use the following as payload:

```json

{

"ticker": "[[ticker]]",

"action": "[[strategy_order_action]]",

"sentiment": "[[strategy_market_position]]",

"quantity": "1",

"price": "[[strategy_order_price]]",

"time": "[[timenow]]",

"interval": "[[timeframe]]"

}

```

For `quantity` use your preffered position sizing based on your money management rules.

See the following docs for more information about [TradersPost](https://docs.traderspost.io/docs).

#### For Futures [#for-futures]

When setting a strategy alert for futures you plan on automating TradersPost recommends for the current contract traded to be provided.

The futures contract should be in the format `[ROOT][MONTH CODE][4 digit YEAR]`. This can be provided using this template:

```json

{

"ticker": "[[current_contract_myyyy]]",

"action": "[[strategy_order_action]]",

"sentiment": "[[strategy_market_position]]",

"quantity": "1",

"price": "[[strategy_order_price]]",

"time": "[[timenow]]",

"interval": "[[timeframe]]"

}

```

### 3commas [#3commas]

#### Single Webhook [#single-webhook]

Create a new signal bot on 3commas, select TradingView strategy, and copy the provided URL.

In the LuxAlgo strategy alert creation menu create a new webhook, add the provided webhook URL, and use the following as payload:

```json

{

"secret": "your_secret_token",

"max_lag": "300",

"timestamp": "[[timenow]]",

"trigger_price": "[[strategy_order_price]]",

"tv_exchange": "[[exchange]]",

"tv_instrument": "[[ticker]]",

"action": "[[strategy_order_action]]",

"bot_uuid": "your_bot_uuid",

"strategy_info": {

"market_position": "[[strategy_market_position]]",

"market_position_size": "1"

},

"order": {

"amount": "1",

"currency_type": "base"

}

}

```

Use your provided "secret" and "bot\_uuid".

For `amount` in `order` use your preffered position sizing based on your money management rules.

See the following [docs](https://help.3commas.io/en/articles/8778456-signal-bot-tradingview-strategy-type) to learn more about 3commas strategy bots.

#### Multiple Webhooks [#multiple-webhooks]

You can also use multiple webhooks with 3commas to open specific positions.

Create a new signal bot on 3commas, select custom signal, select "Reversal" as direction, copy the provided URL and use the following payloads depending on the position:

Only keep "long" enabled in the event tab.

```json

{

"secret": "your_secret_token",

"max_lag": "300",

"timestamp": "[[timenow]]",

"trigger_price": "[[strategy_order_price]]",

"tv_exchange": "[[exchange]]",

"tv_instrument": "[[ticker]]",

"action": "enter_long",

"bot_uuid": "your_bot_uuid"

}

```

Only keep "exit long" enabled in the event tab.

```json

{

"secret": "your_secret_token",

"max_lag": "300",

"timestamp": "[[timenow]]",

"trigger_price": "[[strategy_order_price]]",

"tv_exchange": "[[exchange]]",

"tv_instrument": "[[ticker]]",

"action": "exit_long",

"bot_uuid": "your_bot_uuid"

}

```

Only keep "short" enabled in the event tab.

```json

{

"secret": "your_secret_token",

"max_lag": "300",

"timestamp": "[[timenow]]",

"trigger_price": "[[strategy_order_price]]",

"tv_exchange": "[[exchange]]",

"tv_instrument": "[[ticker]]",

"action": "enter_short",

"bot_uuid": "your_bot_uuid"

}

```

Only keep "exit short" enabled in the event tab.

```json

{

"secret": "your_secret_token",

"max_lag": "300",

"timestamp": "[[timenow]]",

"trigger_price": "[[strategy_order_price]]",

"tv_exchange": "[[exchange]]",

"tv_instrument": "[[ticker]]",

"action": "exit_short",

"bot_uuid": "your_bot_uuid"

}

```

Use your provided "secret" and "bot\_uuid".

See the following [docs](https://help.3commas.io/en/articles/8529406-signal-bot-custom-signal-type) to learn more about 3commas signal bots.

### Cornix [#cornix]

Go to your dashboard, and create a new bot by selecting "TradingView Bot".

Select wether this bot should be for live or a demo trading account.

Configure the bot name, account, symbol, position size and the direction.

Click on create bot and choose in the new window if the bot should be activated or not after creation. If not activated you will need to activate it later on.

Once created copy the Webhook URL for this bot and paste it in the webhook URL field in the LuxAlgo alert creation menu.

Before creating the alert only keep the relevant event enabled based on the direction selected before, if you selected "Long" only keep the long event selected.

Repeat the above steps for the Short direction.

### Discord [#discord]

You can receive messages from AI strategy alerts directly in your Discord server, this can be useful to have a personal log for alerts or just a simple place to get notified on actions taken by strategies.

Make sure you have a server and a channel with a webhoook setup, to learn more about creating webhooks for Discord see [this](https://support.discord.com/hc/en-us/articles/228383668-Intro-to-Webhooks) guide.

Copy the webhook URL, paste it in the webhook URL field in the LuxAlgo alert creation menu, and use the following payload:

```json

{

"username": "[[strategy_name]]",

"content": "New [[strategy_event]] signal on [[ticker]] ([[timeframe]]m)"

}

```

You maye customize the message look using the fields described [here](https://discord.com/developers/docs/resources/webhook#execute-webhook-jsonform-params).

# How To Use Discord (/docs/getting-started/community)

Discord is a free instant-messaging platform for participating in communities. Below you will find the basics on how to create a free Discord account and how to get access as a LuxAlgo subscriber.

This is the platform where we host our 150,000+ member community with automated alerts, strategy forums, and various bots to further optimize your experience at LuxAlgo.

## Create A Free Discord Account [#create-a-free-discord-account]

To create a Discord account go to the [Discord website](https://discord.com), download the Discord app (or open it from the browser) and enter your desired username.

## Joining The Discord [#joining-the-discord]

When you first join our server, you won't be able to see anything besides our public channels. You can get help in the **#support** channel, see our announcements, get useful information regarding LuxAlgo, and learn how to sign up. If you haven't already joined the server, [click here.](https://discord.gg/lux)

## Exclusive Roles [#exclusive-roles]

Once you get a subscription on our website, you will be able to connect your Discord account to our system, which will give you exclusive perks.

The @Premium, and @Ultimate Discord roles are automatically granted to users depending on the plan they chose from [our website](https://luxalgo.com/pricing). All users are prompted to connect their Discord account right after they sign up for their roles, however, we also send an email which includes a link to your LuxAlgo account anyone can always access to connect their Discord account and receive an exclusive role.

Every exclusive role includes access to our highly active community market discussion channels where traders discuss all markets using LuxAlgo tools alongside a user strategy forum for sharing trading strategies made with our exclusive tools, and an Alert Scripting forum for sharing advanced alert setups from our toolkits with the powerful Alert Scripting feature.

Our community also has scanner alerts which are made up of thousands of pre-set alerts using our exclusive toolkits.

The @Premium and @Ultimate roles unlock access to all of our scanner alerts which are also based on features from our Signals & Overlays toolkit.

The @Ultimate role includes access to a section of channels for backtesting, where our data-driven traders discuss strategy creation & share backtesting data using our AI Backtesting Assistant.

To get your exclusive role, click "Connect Accounts" from your Subscription Confirmation email and then click the 'Authorize Discord' button in the portal and your role will be granted automatically.

If you are having trouble, please reply to the Subscription Confirmation email with your Discord username and our support team will ensure you have full access right away.

# FAQ (/docs/getting-started/faq)

## Access [#access]

Sign up to any plan on

[our website](https://luxalgo.com)

.

After purchasing a subscription, you will be prompted to

**connect your accounts**

& get instant access.

If you are having trouble, let our live human support team know your TradingView username and we will fix your access. If you're speaking to an AI Agent, request to speak to a human directly.

The **Premium Plan** gives you the full set of our world-renowned Price Action Concepts®, Signals & Overlays®, and Oscillator Matrix® toolkits + screeners on TradingView which makes it the best choice for advanced technical analysis.

The **Ultimate Plan** was designed for using our AI Backtesting platform and Backtesters, allowing you to automate backtesting of our toolkits. This is the most popular choice as it uses AI & deep optimization to give you the biggest advantage possible for data-driven, automated analysis.

Make sure the username you used to connect your TradingView account is correct. If so, **refresh your browser/app** and then check your your Indicators --> Invite-only scripts folder on TradingView again.

If you just created a TradingView account as you signed up for a LuxAlgo core platform subscription, it may take 5 - 10 minutes to be indexed in TradingView's userbase first. Please wait and then try entering your username again within our Connect Accounts user portal.

If you still don't have access, let our live human support team know your TradingView username and we will fix your access. If you're speaking to an AI Agent, request to speak to a human directly.

## Products [#products]

Our tools are designed to work across all major asset classes and timeframes, but the specific coverage depends on which platform you are using:

TradingView Indicators (Premium Plan): These tools function on any ticker and timeframe available on TradingView. Whether you are trading obscure altcoins, penny stocks, or futures on a 1-minute chart, the indicators will load and provide analysis instantly.

LuxAlgo AI (Ultimate Plan): Our AI platform scans and backtests strategies on major liquid markets including Crypto (BTC, ETH, SOL, etc.), Forex (EURUSD, GBPUSD, etc.), Indices (SPX, NDX), and major Stocks. It is optimized for standard timeframes (5m, 15m, 1H, 4H, Daily) to find the most robust strategies for Scalping, Swing Trading, or Day Trading.

No, all features within our toolkits do **not** repaint. Everything appears in real-time and are confirmed & permanent on the chart once the candle a signal was generated on has closed.

Repainting is where past results of an indicator or a signal change based on data in the future. In terms of our exclusive tools, none of them repaint in any way. Only a small few of our hundreds of free indicators have this functionality.

Within our Signals & Overlays toolkit, any signal is confirmed only once the candle is closed. This means a signal could appear on your chart but not be confirmed until that candle is closed and the next candle has started.

Our alerts in Discord will **never** notify you on any signal until the candle has closed and confirmed it. If you're adding alerts for our toolkits within TradingView, make sure to always select the "Once per bar close" configuration.

You don't need to upgrade your TradingView account, our exclusive tools work with 100% functionality on the basic plan of TradingView (free). [You can sign up for free here](https://www.tradingview.com/gopro/?share_your_love=LuxAlgo).

Yes, all of our plans are great for beginners.

Every plan comes with many tutorials as well as access to our highly active community where users can get 24/7 support, discuss strategies, & go through daily analysis amongst each other using LuxAlgo.

Our Ultimate Plan is great for traders who want to do more powerful strategy creation but even a beginner can maximize their advantage of it using our AI platform.

Yes, you can automate your trades using LuxAlgo. Our LuxAlgo AI platform is specifically designed for algorithmic trading, allowing you to generate backtested strategies and stream live signals directly to third-party automation platforms via webhooks.

Additionally, our indicators and strategies available on TradingView can be automated in the same way by setting up alerts that trigger webhooks. However, for the most robust experience, we recommend using our AI strategies which are engineered specifically for generating automated signals.

Yes, you can send trades to MetaTrader via third parties.

While our premium visual indicators (like Signals & Overlays™) are designed exclusively for the TradingView charting interface, you can still execute trades on your MT4 or MT5 account using our tools:

For Automation (Recommended): You can use the LuxAlgo AI platform to generate strategies and stream signals directly to third party apps that plug in to your MetaTrader account via webhooks. This allows you to run algorithmic strategies on our platform while the trades execute automatically on yours.

For Manual Trading: Many users perform their analysis on TradingView using our premium toolkits and then manually enter the resulting trades into their MetaTrader terminal.

Yes, TradingView supports real-time data for the majority of tickers you can find on the platform. Only a small portion of them (mostly futures contracts) require a small monthly fee to access real-time data.

While we are proud to be the world's largest provider of free open-source indicators on TradingView, our paid plans offer a completely different level of professional capability:

LuxAlgo AI (Ultimate): The biggest difference is our AI platform, which goes beyond simple indicators. It allows you to generate backtested strategies, optimize settings using data-driven insights, and automate your trading via webhooks—capabilities that do not exist in free scripts.

Premium Toolkits: Our paid indicators (like Signals & Overlays and Price Action Concepts) are designed as "all-in-one" systems with extreme capabilities for customization & alert functionalities. Instead of combining multiple free indicators that clutter your chart, these toolkits provide comprehensive, noise-free workflows with advanced features and customization specifically engineered for serious traders.

This error message appears when an user does not have access to the indicator. If you've already registered your TradingView username within our Connect Accounts portal and you're seeing this message, refresh your browser or app and make sure you're logged in on the TradingView profile you entered.

If you are still getting this issue, let our live human support team know your TradingView username and we will fix your access. If you're speaking to an AI Agent, request to speak to a human directly. If you have not signed up with us, you'll see this error when trying to add our exclusive tools to your chart. You can get instant access [here](https://luxalgo.com/pricing).

This error generally occurs when TradingView can't handle script loads under high traffic. This error can appear when a high number of features are enabled. Changing settings within the indicators, or hiding/unhiding it will make the script recalculate and potentially fix the issue.

We are always trying to improve the performance of the toolkit in order to limit these issues.

This error generally occurs when a TradingView study exceeds the memory limit fixed by TradingView. This error can't be directly prevented and will generally be returned when using anything below the 1 minute timeframe.

We recommend users to stay with minute and higher timeframes to avoid potential errors with our premium toolkits.

## Billing [#billing]

You can cancel your subscription anytime by logging directly into your account on [our website](https://luxalgo.com/account/) and accessing the billing page where you will find your subscription and a way to easily cancel it on your own.

Once your subscription has been canceled, you will have access for the rest of the time in the plan you purchased and you will not be charged again.

You can re-activate a subscription that you previously cancelled by purchasing a plan again on our [pricing page](https://luxalgo.com/pricing).

Once you select the plan you want to subscribe back with, make sure to login to the same account you used with your previous subscription.

You can upgrade your subscription by logging in on [our website](https://luxalgo.com/pricing).

Once logged in, select your plan of choice to upgrade to and you will see a pop-up modal with the details.

We automatically convert any remaining time into a value of days on your new plan so you have a longer period of time on your newly upgraded subscription.

You can extend your current subscription up to 3 times on [our website](https://luxalgo.com/pricing).

Keep in mind that we only allow extending a subscription 3 times and it is for annual plans only.

For special limited time offers we do you can receive discounts which are all automatically applied, displayed on the pricing cards, and for the first payment of your subscription only.

You can always get up to 50% off the total price you'd pay monthly by choosing to pay annually on our plans.

We offer a 30 day money back guarantee so you can try our exclusive tools for 30 days risk free. We also have hundreds of free indicators you can try on our [Library](https://luxalgo.com/library) to experience our free tools first.

No, the price you signed up for is the price you will keep forever as long as you stay signed up. We will **never** change the price of your subscription. All members are grandfathered into the price they first signed up at regardless of any price increases we may do in the future.

Please keep in mind that all coupons used on LuxAlgo.com are for the first interval of your subscription only. All future billing intervals aside from the first one will be at the full price of the subscription you chose.

Access is instant for both our AI platform and TradingView tools immediately after sign-up:

LuxAlgo AI Platform: You can log in directly on our website to access the AI strategies immediately.

Complimentary TradingView tools: You will be prompted to enter your TradingView username in our Connect Accounts portal. Once connected, our Premium toolkits will instantly appear in your TradingView account under the "Invite-only scripts" folder (found within the Indicators menu on TradingView).

Troubleshooting: If you don't see the indicators on TradingView right away, try refreshing your browser or app. If you are still having trouble, please use the Live Chat on our website (request to speak to a human) or reply to your confirmation email, and our team will resolve it immediately.

If you're within 30 days of your first initial purchase, you can request a refund by getting in touch with our live human support team from contacting [support@luxalgo.com](mailto:support@luxalgo.com) or by requesting to speak to a human if you've already reached out on our website so a team member can help you with this directly.

Within your account, you can optionally downgrade your plan which will only start once your current plan ends.

For example if you have 15 days left in your Ultimate Plan and you're downgrading to Premium, the Premium plan will start in 15 days at full price.

Yes, we allow username changes in most scenarios as long as it's not too frequent. You may request this and send your new username alongside your old username to [support@luxalgo.com](mailto:support@luxalgo.com) and you may need to ask for our live human support team and we will change your username. If you're speaking to an AI Agent, request to speak to a human directly for this request.

# How To Get Updates (/docs/getting-started/how-to-update)

## Applying An Update [#applying-an-update]

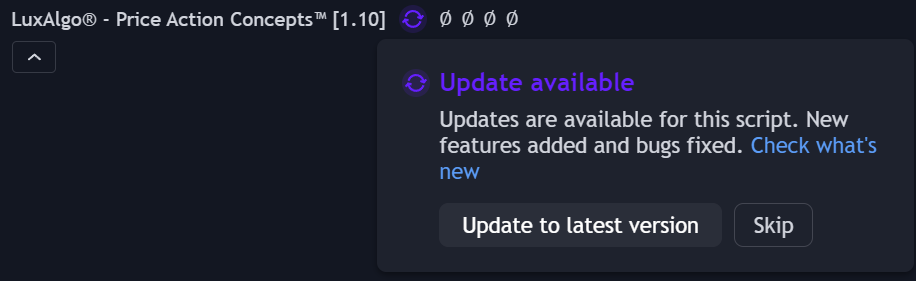

On Tradingview updates are easy to apply. Once an update is available, refresh your chart, then a purple 🔄 icon will be visible near the indicator title, click on it and click on "Update to latest version".

You can also apply an update by following these steps:

1. Refresh your browser or mobile app

2. Remove the indicator from your chart

3. Re-add it from your invite-only indicators

The latest version of the indicator should appear.

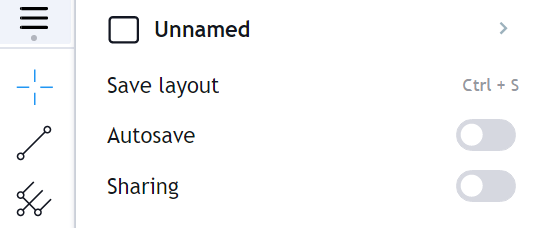

Make sure to save your **Chart Layout** on Tradingview after successfully installing an update so you can ensure it will stay

## Receiving Updates Notifications [#receiving-updates-notifications]

We always announce our updates on our community Discord server & [X Account](https://x.com/LuxAlgo). You can also receive update notifications on your TradingView charts directly by going to:

`settings -> notifications -> SCRIPTS YOU'VE ADDED TO FAVORITES OR LIKED`

Make sure to follow the LuxAlgo account on [TradingView](https://www.tradingview.com/u/LuxAlgo/#published-scripts) to ensure you are notified when we push updates with new features to our exclusive tools!

# Quickstart (/docs/getting-started/introduction)

## Getting Started with LuxAlgo [#getting-started-with-luxalgo]

Welcome to the LuxAlgo documentation guide. Click any of the buttons below to learn how to get setup, use our tools, and enhance your trading experience.

In-depth guide on how to use Quant, our coding agent for creating indicators and strategies using Pine Script®.

In-depth guide on how to use our Toolkits

In-depth guide on how to use our Screeners

In-depth guide on our Backtesters

Learn how to find strategies using our AI platform.

Get alerted from AI strategy trades.

Learn how to setup exclusive LuxAlgo tools on TradingView

## Frequently Asked Questions [#frequently-asked-questions]

Need quick answers to general questions about our website, products, or billing? Click the button below to visit our FAQ.

Read through our frequently asked questions

## Join our Community [#join-our-community]

Need further support or want to give us some feedback? You can [join our community](https://discord.com/invite/LUX) or drop us an email at [support@luxalgo.com](mailto:support@luxalgo.com).

# How To Setup LuxAlgo (/docs/getting-started/setup-tools)

Once you've signed up to any plan on [our website](https://luxalgo.com/pricing) -- you will be able to see a place to "Connect Accounts" and enter your TradingView username to get instant access to use our exclusive tools compatible with TradingView.

In order to use our exclusive tools, you need to open a chart on TradingView.

Once your chart is open, click on **Indicators** (or type **/** ) to open the indicator menu, then click on "**Invite-only Scripts**". You should see the names of each Toolkit, Screener, or Backtester appear in this folder and you can click on one them to add to your chart.

Remember, you don't need to use all of these tools at once. It is suggested for users to explore through our tools to find a couple features that fit most optimally in your trading.

If you don't see the invite-only scripts folder or the locks appear red, please first try refreshing your browser/app. If this still doesn't have them show up, please email [support@luxalgo.com](mailto:support@luxalgo.com) with your TradingView username or contact live-chat on our website and our team will grant you access right away.

If you want to quickly access our tools you can add them to your favorites by clicking on the star at the right of their names in the folder. You will then be able to load the starred indicators directly from your favorites tab while on your charts.

# TradingView Alerts (/docs/getting-started/tradingview-alerts)

In this page, we show you the specifics of how to set up any alert on TradingView in general. If you want to learn how to set up specific alerts on our exclusive tools specifically, you can see the following [video](https://youtu.be/olKQq5XR5S0?t=38).

On the TradingView platform, alerts can be created to trigger for any user set condition, such as crosses between two indicators, price entering or exiting a channel...etc. Users can be notified when the condition is trigerred via phone notifications, emails, SMS, and more through webhooks.

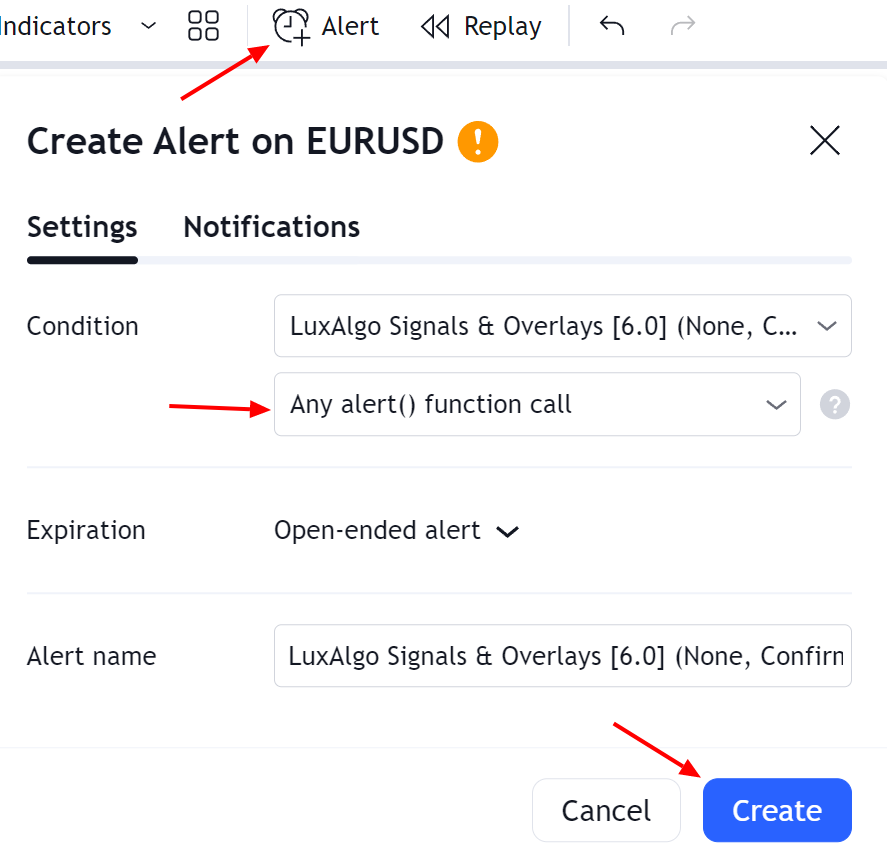

## How To Create An Alert [#how-to-create-an-alert]

To create an alert you can:

* Click on the alert button at the top of your chart.

* From the alert manager

* Using hotkeys `ALT + A` (Windows) or `⌥ + A` (Mac)

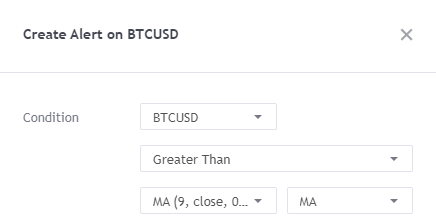

## Trigger Conditions [#trigger-conditions]

Users can select the conditions used to trigger an alert in the condition menu, selecting the indicators and a set of rules used to trigger an alert. The second drop down menu controls the specific alert trigger conditions, while the other drop down controls the elements/plots to be used for conditions.

Indicators return plots, which are visual elements that can be used to set the alert condition. Plots are used to visualize series of values, conditions, etc. Note that indicators can return multiple plots.

Available conditions to set custom alerts are explained below:

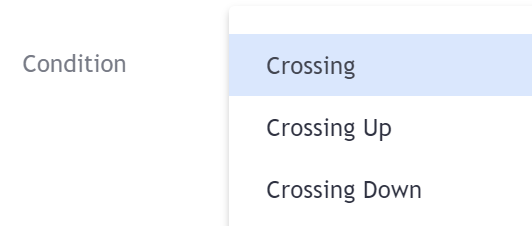

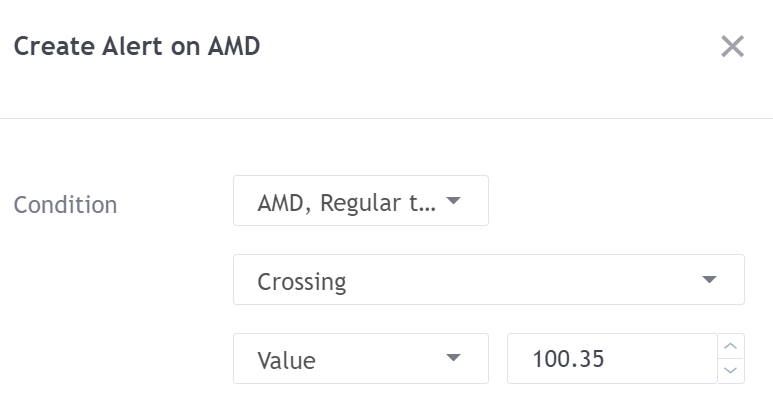

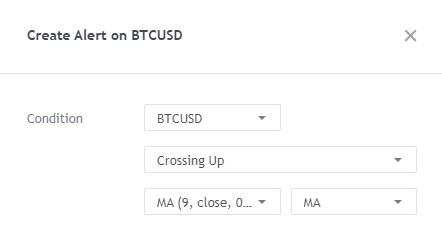

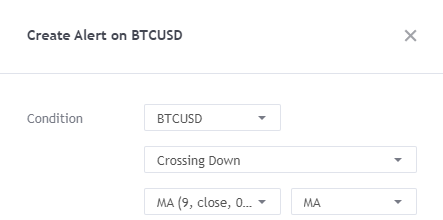

### Crossing/Crossing Up/Crossing Down [#crossingcrossing-upcrossing-down]

Crossing conditions are commonly used and allow users to be alerted when two elements cross each other.

Three crossing conditions are available, **Crossing**, **Crossing Up**, **Crossing Down**.

**Crossing** will alert on any crosses between two selected plots/values.

**Crossing Up** will alert only when the first selected element crosses over the second one.

**Crossing Down** will alert only when the first selected element crosses over the second one.

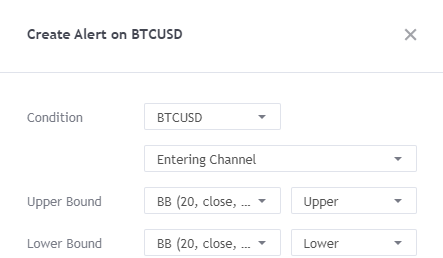

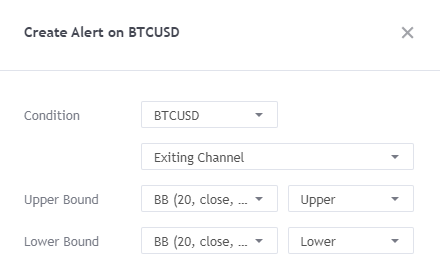

### Entering/Exiting Channel [#enteringexiting-channel]

**Entering/Exiting Channels** conditions will trigger when any selected element enter or exit user selected upper/lower bounds.

The **Entering Channel** condition will trigger when the element in the first drop-down menu cross-under the selected upper bound or cross-over the selected lower bound.

The **Exiting Channel** condition will trigger when the element in the first drop-down menu cross-over the selected upper bound or cross-under the selected lower bound.

### Outside/Inside Channel [#outsideinside-channel]

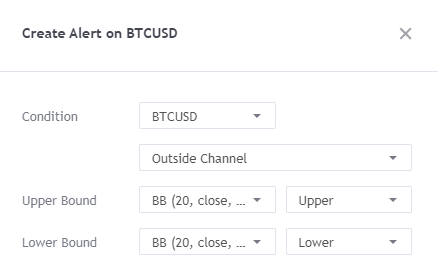

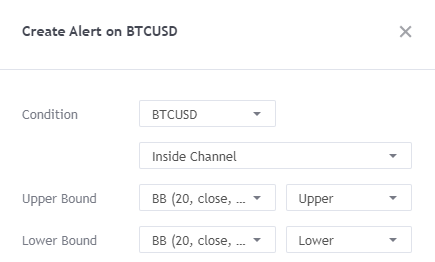

**Outside/Inside Channels** conditions will trigger when any selected element is outside or within selected upper/lower bounds.

### Greater/Less Than [#greaterless-than]

The **Greater Than** and **Less Than** conditions will trigger when a selected element is greater or less than a selected element or value.

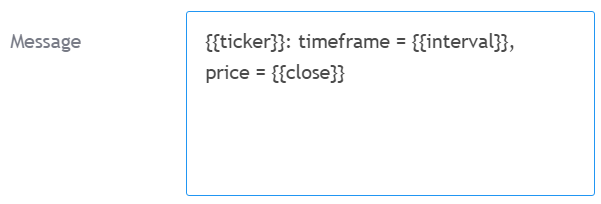

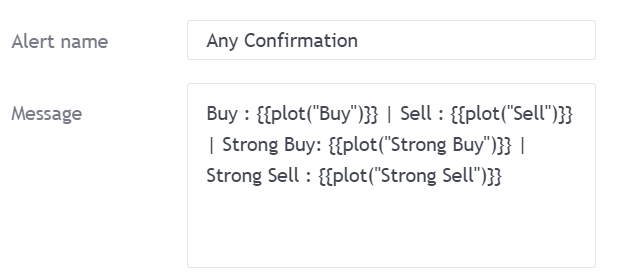

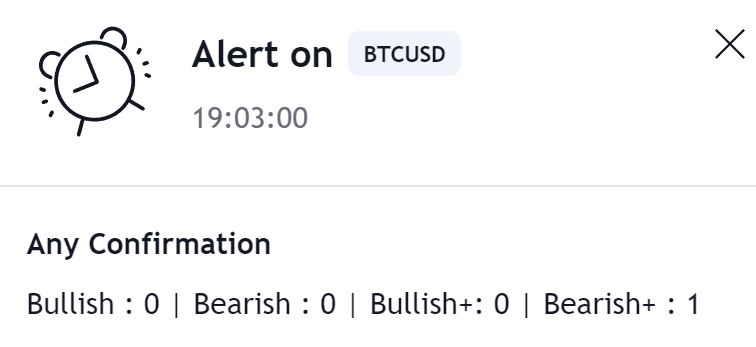

## How To Use Placeholders [#how-to-use-placeholders]

Placeholders allow for the value of a variable to be returned in an alert message. This variable can be the closing price of a symbol (`{{close}}`), the time frame of the chart the alert is created on (`{{interval}}`), and even the value of an indicator. This is done using the `{{plot("Name")}}` placeholder, where `"Name"` is the name of the plot you want the value to be returned in the alert message. Note that only the first 22 plots in an indicator can be used in placeholders.

Note that `plot("Name")` must be part of the indicator selected in the alert condition.

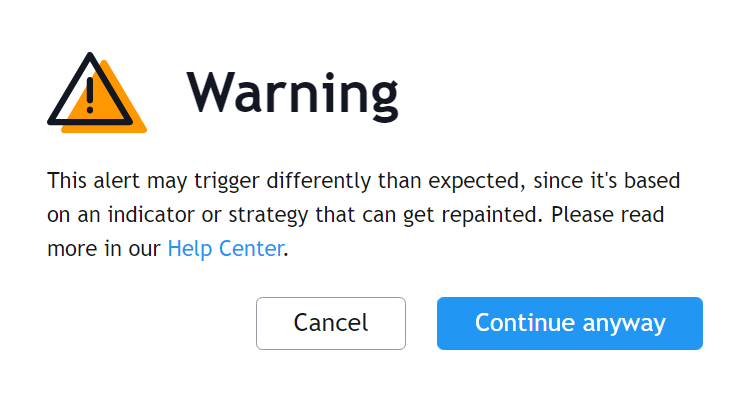

## Warning Message [#warning-message]

When you create an alert using certain indicators such as the Signals & Overlays® indicator, you might see a warning message, this is caused by internal Pine Script® functions used in the script that may have a repainting behavior when set in a specific way.

The alerts provided by the LuxAlgo indicators **do not repaint** and as such, you can click on **continue anyway**.

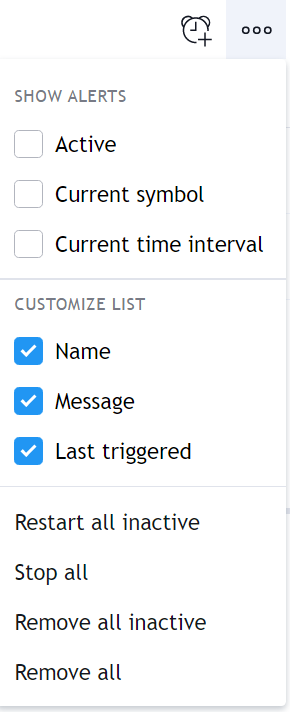

## Managing Alerts [#managing-alerts]

The alerts manager menu allows you to manage the alerts you have currently set. From there you can create, remove, pause, reactivate, clone, search, sort and edit your alerts. To access the alert manager menu click on the alerts icon represented by an alarm symbol at the top left of the chart.

If you want to remove all your current alerts click on the three horizontal dots at the right of the "add alert" icon, then select "remove all".

For more information on how to manage alerts go [here](https://www.tradingview.com/support/solutions/43000595311-manage-alerts/).

### Updating Alerts [#updating-alerts]

It is important to note that if one of the indicator settings is **changed after the alert is created**, then the alert will be **triggered using the old settings**. In order to update an alert go to the alert manager and click on edit.

In the first drop-down menu of the **Condition** section, select the second indicator with the same name as the one first used to create the alert you want to update and save the alert.

# What Is TradingView? (/docs/getting-started/tradingview)

[TradingView ](https://www.tradingview.com)is a free charting platform and social network where traders/investors can **look** at financial charts and use a wide variety of tools to spot opportunity in every market across Stocks, Forex, Crypto, Futures & Commodities. TradingView users can connect most brokers to trade directly on the platform and **leap** into opportunities as they are presented in real time from their charts.

This is the platform where we host our exclusive tools. You can create a free account on TradingView and then sign up on [our website](https://luxalgo.com/pricing) to receive instant-access to use our tools.

## How To Create A TradingView Account [#how-to-create-a-tradingview-account]

In order to create a TradingView account, you need to go to the TradingView [homepage](https://www.tradingview.com). Click on "Sign in" at the top right of the homepage, then click on "Sign up" at the bottom of the current window. You can sign up using your social media profiles or an email address.

## TradingView Charts [#tradingview-charts]

### How To Open A Chart On TradingView [#how-to-open-a-chart-on-tradingview]

You can open a chart on TradingView by clicking on 'Chart', located at the top left of the website when you are logged in.

### How To Change Symbol [#how-to-change-symbol]

You can change the symbol of the chart by clicking on the top left section containing the current chart ticker.

You can also directly type the name of the symbol on your keyboard.

Once you click on it, you will be able to search for specific symbols. You can also filter out symbols by markets or exchange.

### Change Chart Timeframe [#change-chart-timeframe]

Timeframes determine the frequency at which a new candle is displayed on the chart. To change the timeframe of your chart simply click on the section at the right of the ticker name and select a timeframe of interest.

You can also type the timeframe directly on your keyboard to change it.

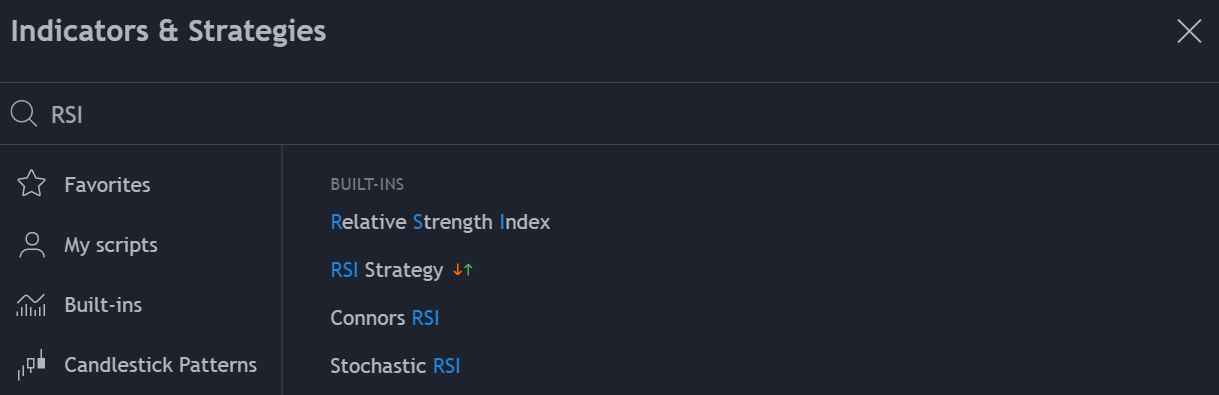

### Add Indicators To Your Chart [#add-indicators-to-your-chart]

Click on the **Indicators** button at the top of the chart. This will open a menu where you can search for the indicator and click on it to add it to your chart.

### Save A Chart Layout [#save-a-chart-layout]

You can create, delete and save chart layouts on TradingView if you wish to save your indicator & chart settings on specific tickers/timeframes. Once you make a change on a layout, you will need to save these changes, all you need to do is to click on the cloud symbol at the top right of the chart.

You can also save a chart layout by pressing `ctrl + s` or `cmd + s` for mac users, on your keyboard.

# What Is LuxAlgo? (/docs/getting-started/what-is-luxalgo)

LuxAlgo is the leading AI platform for generating indicators and trading strategies.

We are widely known for hosting the world’s largest open-source [Library](https://luxalgo.com/library) of trading indicators & algorithms used by millions of traders across 5+ charting platforms such as TradingView, however, this massive repository serves a higher purpose. It acts as the intelligence engine that powers our advanced AI platform for indicators and strategy creation.

We constantly automate technical analysis concepts traders use into scripts, innovate on them by building advanced algorithms, and package all of them into a streamlined AI platform. An ecosystem where traders can easily generate smarter, statistically robust strategies of their own rather than relying on someone elses research or market "edge".

## Architect Your Edge [#architect-your-edge]